Finally Friday Reads: False Ethos and Pathos rule the Media and Politics

Posted: April 24, 2026 Filed under: Foreign Affairs, Republican politics, U.S. Economy, U.S. Politics | Tags: @johnbuss.bsky.social John Buss, Drunk Kash Patel, Federal Reserve Bank, Jerome Powell, Lincoln Memorial reflecting pool, RFK Jr Zoophilia Weirdo 11 Comments

“Meanwhile, early this morning somewhere near Nashville…” John Buss, repeat1968,

Good Day, Sky Dancers!

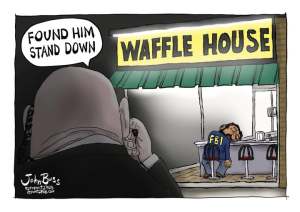

The headlines are yet another mash-up of feelings run amok and logic gone awry. Another week has passed, and I don’t regret getting rid of cable and most forms of TV news. It’s just all one big tabloid of rampant stupidity. Here’s a great headline from The Intercept about our nation’s FBI Director. “Kash Patel Got Arrested for Public Urination After a Night of Drinking. The FBI director was arrested twice in his youth for alcohol-related incidents that he said were “not representative of my usual conduct.”

It’s another sign of why Republicans never do any due diligence when running committee hearings to affirm Federal Office holders in the highest offices in the nation. They’re a psychiatrist’ nightmare.

Eventually, some independent news agency catches up to them, and we read about it on the internet news stream, which is a hash of conspiracy theories and the hard work of a few good reporters. This story is reported by Trevor Aaronson.

FBI Director Kash Patel was twice arrested in incidents involving alcohol, once for public intoxication and once for public urination after leaving a bar, he admitted in a 2005 letter about disclosures on his Florida Bar application.

The letter obtained by The Intercept was part of Patel’s personnel file at the Miami-Dade Public Defender’s Office, where he once worked. The document, written “per instructions of my employer,” describes incidents of alcohol-related indiscretions not uncommon for those in their teens and twenties.

Two decades later, as Patel pushes back against allegations that drinking is impairing his leadership of the nation’s top law enforcement agency, these arrests show how Patel’s alcohol use has been subjected to scrutiny before in his professional life.

One incident recounted by Patel occurred in 2005, about four months before he wrote the letter. At the time, he was a law student at Pace University in New York celebrating with friends.

“We went to a few of the local bars and consumed some alcoholic drinks,” he wrote.

When they walked home, they made a bad decision.

“In a gross deviation from appropriate conduct, we attempted to relieve our bladders while walking home,” Patel said in the letter. “Before we could even do so, a police cruiser stopped the group. We were then arrested for public urination.”

Patel paid a fine after the incident, he wrote in the letter.

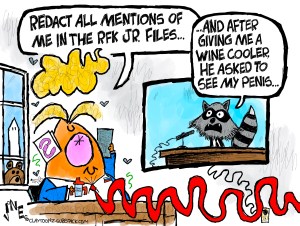

That’s still nothing compared to the stories we heard about dead animals and RFK Jr. This is from one of last week’s editions of The Guardian. I suppose I no longer need to explain that when I write these blog posts, they are surrounded by political cartoons, not beautiful artwork or actual photos anymore. I prefer animated Scheudenfrade. “RFK Jr once cut penis off ‘road-killed raccoon’ in New York, new book reveals. Health secretary in a diary entry said his kids were in the car as he cut off animal’s genitals in 2001 to ‘study them later’.”

That’s still nothing compared to the stories we heard about dead animals and RFK Jr. This is from one of last week’s editions of The Guardian. I suppose I no longer need to explain that when I write these blog posts, they are surrounded by political cartoons, not beautiful artwork or actual photos anymore. I prefer animated Scheudenfrade. “RFK Jr once cut penis off ‘road-killed raccoon’ in New York, new book reveals. Health secretary in a diary entry said his kids were in the car as he cut off animal’s genitals in 2001 to ‘study them later’.”

Don’t worry, I’ll keep this brief. Buddha bless the entire Guardian staff that had to work on this one.

Robert F Kennedy Jr once cut the penis off a road-killed raccoon in an incident that is just one of several involving dead animals that the controversial US health secretary has been involved in.

A new book called RFK Jr: The Fall and Rise was published this week and reveals a diary entry for Kennedy that describes the prominent vaccine critic and leader of the “Make America healthy again” (Maha) movement stopping his car on a New York highway on 11 November 2001.

“I was standing in front of my parked car on I-684 cutting the penis out of a road killed raccoon, thinking about how weird some of my family members have turned out to be,” Kennedy wrote in the journal.

He added: “My kids waited patiently in the car.”

Isabel Vincent, the author of the new book, told People that he took the raccoon’s genitals so he could “study them later”.

Kennedy has long had a fascination for animal bodies, especially those he finds dead which he sometimes collects and studies. Elsewhere in the book, the author notes that a journalist traveling with Kennedy in Long Island in 2001 reported that he was fascinated by dead seagull corpses.

“I’d like to pick up some of these dead seagulls for my skull collection,” the book quotes Kennedy as saying, though his schedule on the day did not allow him to pause his journey and harvest the bones.

There have been numerous stories involving Kennedy and his treatment of dead animals.

Environmental groups were outraged over a story which revealed the former presidential candidate once severed the head of a washed-up deceased whale with a chainsaw and strapped it to his car’s roof. He also once confessed to dumping a dead bear cub in New York’s Central Park, attempting to make it look like the creature was killed by a bicyclist.

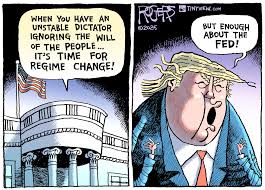

Meanwhile, hardworking, competent Federal officials get the nuisance-lawsuit treatment. This is from the Associated Press. “Justice Department drops criminal probe of Fed chair Powell, likely clearing the way for Warsh.” It’s really difficult to see how normal people stay sane and hold their offices in this environment.

Meanwhile, hardworking, competent Federal officials get the nuisance-lawsuit treatment. This is from the Associated Press. “Justice Department drops criminal probe of Fed chair Powell, likely clearing the way for Warsh.” It’s really difficult to see how normal people stay sane and hold their offices in this environment.

The Justice Department has ended its investigation into Federal Reserve chair Jerome Powell, clearing a major roadblock to the confirmation of Kevin Warsh as his successor.

U.S. Attorney for the District of Columbia Jeannine Pirro said on X on Friday that her office was ending its probe into the Fed’s extensive building renovations because the Fed’s inspector general would scrutinize them instead.

The move could lead to a swift confirmation vote by the Senate for Warsh, a former top Fed official whom President Donald Trump, a Republican, nominated in January to replace Powell. Powell’s term as chair ends May 15. Sen. Thom Tillis, a North Carolina Republican, had said he would oppose Warsh until the investigation was resolved, effectively blocking his confirmation.

Republicans praised Warsh during a Tuesday hearing even as Democrats questioned his independence from Trump, the lack of transparency around some of his financial holdings, and what they said was his flip-flopping on interest rates. Still, Trump’s previous appointment to the Fed’s board of governors, Stephen Miran, was approved by the full Senate just 13 days after his nomination.

Investigation lacked evidence, a court says

The probe was among several undertaken by the Justice Department into Trump’s perceived adversaries. For months it had failed to gain traction as prosecutors struggled to articulate a basis to suspect criminal conduct. Other efforts by the department to prosecute Trump’s adversaries, including New York state Attorney General Letitia James, a Democrat, and former FBI Director James Comey, have also been unsuccessful.

A prosecutor handling the Powell case conceded at a closed-door court hearing in March that the government hadn’t found any evidence of a crime, and a judge subsequently quashed subpoenas issued to the Federal Reserve. The judge, James Boasberg, said prosecutors had produced “essentially zero evidence” to suspect Powell of a crime. Boasberg branded prosecutors’ justification for the subpoenas as “thin and unsubstantiated.”

Speaking of the Republican-based press, base, and politicians peddling one conspiracy theory after another, we see that Tucker Carlson may have gone one too far. I would have never thought that possible, given their depths of depravity and idiocy. This is from The Hill. The analysis and opinions are provided by Matt Lewis.”Trump lived by the conspiracy theory — now he pays the price.” This is basically a class in Karma 101.

Speaking of the Republican-based press, base, and politicians peddling one conspiracy theory after another, we see that Tucker Carlson may have gone one too far. I would have never thought that possible, given their depths of depravity and idiocy. This is from The Hill. The analysis and opinions are provided by Matt Lewis.”Trump lived by the conspiracy theory — now he pays the price.” This is basically a class in Karma 101.

A truism of life — right up there with “don’t read the comments” — is that what goes around comes around. Put another way, if you live by the sword, you will eventually die by the sword.

For more than a decade, these maxims didn’t seem to apply to President Trump — a man who once strongly suggested that Barack Obama had not been born in America, that the 2020 election was stolen, and that Haitian immigrants in Ohio were eating dogs and cats, just to name a few of his whoppers.

To be sure, Trump defenders will note that Democratic conspiracy theories (“Russia-gate,” for example) have also been aimed at Trump. Yes, but Trump legitimately invited scrutiny, and credible analyses rejected the most extreme conclusions anyway — for example, the existence of a “pee tape” or the notion that Russia somehow manipulated election results or otherwise rigged the 2016 election on Trump’s behalf.

Regardless, we have entered a new and possibly ironic phase of the timeline: Trump is finally discovering what it’s like to be on the losing end of a conspiracy theory.

Trump’s failure to release Epstein files was probably the inflection point. But more recently, the conspiratorial thinking about Trump has metastasized.

After Trump cast himself as Jesus on a Truth Social post, some corners of his own political ecosystem began speculating that he might instead be the Antichrist.

Tucker Carlson, for example, went on his podcast and asked, “Could this [Trump] be the Antichrist? Well, who knows? At least that’s my conclusion: Who knows?”

Others settled on demonic possession, which in internet discourse is considered the moderate position.

Michelle Goldberg, writing for the New York Times, has the Tucker story. This from her is an Op-Ed today. “The Conspiracy Theory Behind Tucker Carlson’s Apology.” Who among us ever thought the word apology and Tucker Carlson would appear in the same headline?” He must need money or something.

Michelle Goldberg, writing for the New York Times, has the Tucker story. This from her is an Op-Ed today. “The Conspiracy Theory Behind Tucker Carlson’s Apology.” Who among us ever thought the word apology and Tucker Carlson would appear in the same headline?” He must need money or something.

Tucker Carlson, you might have heard, is sorry. Early this week he posted a long conversation with his brother, Buckley, a former Trump speechwriter, in which they tried to make sense of the wreckage of the second Donald Trump presidency.

“We’re implicated in this, for sure,” said Tucker. A few moments later, he added: “It’s a moment to wrestle with our own consciences. You know, we’ll be tormented by it for a long time. I will be, and I want to say I’m sorry for misleading people.”

For those of us who have spent the past 10 years horror-struck at the mass delusion that Trump is a great man rather than a singularly rapacious and volatile charlatan, Carlson’s words might seem cathartic.

Over the past decade, conservatives have been angrily insisting that our mad emperor is elegantly clothed rather than obscenely naked. Now, finally, there’s growing agreement about his obvious unfitness. Indeed, some former Trump superfans are suddenly wondering if he might be the Antichrist.

I’m all for embracing converts to the anti-Trump cause. But if you listen to the dialogue between Tucker and his brother, it’s clear that rather than honestly reckoning with their role in America’s derangement, they’re developing a new conspiracy theory to explain it away.

Trump, they strongly imply, has been compromised — maybe even blackmailed and physically threatened — by Zionist or globalist forces seeking the deliberate destruction of the United States. On Tucker’s podcast, Buckley described a systematic undermining of America through the George Floyd protests, mass migration and now the war with Iran.

“It can’t be a confluence of random events,” Buckley said. “It is clearly by design. It’s clearly been a long-term plan.”

Can any of you come up with an explanation or some elucidation on WTF is going on here? My vote goes for the rats are leaving the ship. So what better mission for the insane Orange Caligula to come up with during these headlines than yet another way to fuck up yet another National Monument of the utmost historical importance?

Can any of you come up with an explanation or some elucidation on WTF is going on here? My vote goes for the rats are leaving the ship. So what better mission for the insane Orange Caligula to come up with during these headlines than yet another way to fuck up yet another National Monument of the utmost historical importance?

Will the Lincoln Memorial reflecting pool be his next act of cultural devastation? This is from NBC News. “Trump says he’ll renovate ‘filthy’ reflecting pool on National Mall. At an Oval Office event, the president said he’s planning to pour a new surface for the 2,000-foot reflecting pool, giving it an “American flag blue” hue.” Well, at least it isn’t piss gold. Kyla Guilfoil has the lede.

President Donald Trump touted plans Thursday to coat the Lincoln Memorial’s reflecting pool in an “American flag blue” hue, one of his latest construction efforts to refashion government buildings and monuments in Washington, D.C.

Trump said he was inspired to oversee renovations after a friend visited from Germany and noted its decay.

“He said, ‘it’s filthy, dirty. The water is disgusting looking. It’s not representative of the country,'” Trump recalled during a White House event Thursday on drug prices.

He posted a video speaking about the renovation of the more than 2,000-foot-long pool on Truth Social, shortly before his White House event with reporters.

“Right now, it’s got no water in it because it was in terrible shape. It was filthy, dirty, and it leaked like a sieve for many years,” Trump said in the video. “So I actually went over, went with Secret Service and a group of people, and I took, took a look at it.”

The president said there were initial plans to remove the granite in the pool and replace the stone, but that process would have cost $300 million and taken more than three years to complete.

Once again, I sit at my desk and shake my head. It’s a good thing day-drinking was never my thing.

What’s on your Reading, Action, and Blogging list today?

Melt Down Monday: Another Fine Mess Trumplicans got us into

Posted: March 13, 2023 Filed under: just because | Tags: Bank Runs, Bernie Sanders, CryptoCurrency, Dodd-Frank bill, Elizabeth Warren, FDic, Federal Reserve Bank, Flash Digital Bank Runs, Janet Yellen, junk bond king, Katie Porter, SEC, Silicon Valley Bank, US Treasury 15 Comments My body still tells me to say Good Morning!

My body still tells me to say Good Morning!

I’m only on my second cup of coffee while waiting for my Irish Oats to cook. The clock tells me it’s afternoon, but something about me refuses to believe it. Why am I rudely being pushed into a part of the day rather than enjoying my lazy morning and looking forward to my Night Life? The best thing about teaching Grad school is that I no longer teach morning classes. Thanks to Dubya (wrecked the country) Bush, I only have that sacred space with its full glory for about 4 months a year. I’m grading midterms and wading through a seriously unnecessary set of bank failures in a bit of a fog. This is my version of No Exit.

Every time I teach my Grad Derivatives class in the Spring, some unnecessary financial crisis pops up. It’s not a huge one like another thing for which we can thank Dubya (wrecked the economy), Bush, and his cronies. This will not be the next “Great Recession” creator.

The Republicans under Theodore Roosevelt and Ulysses S Grant determined that you cannot trust huge actors in concentrated markets to regulate themselves. They called them trusts back then. They muck things up worse than the regulations while taking advantage of their customers for extraordinary profits until the jig is up. They also lead to substantial negative spillover costs paid for with taxpayer money. Many times, especially with situations like the Norfolk situation, victims of these costs never fully recover their losses. Real economists know this. It’s why Republicans haven’t had one around since Bernanke.

I wrote extensively about why the financial system ran amok and wrecked the economy around 2008. I am again writing about a very similar situation. Much of it’s rooted in the chipping away of protections set up to protect us from a recurrence of the Great Recession removed by Trump, the Republicans, and any elected official that basically gets vast donations from Wall Street and Banks. NBC News Sahil Kapur follows the ties between that and what’s happening now. “Silicon Valley Bank collapse puts new spotlight on a 2018 bank deregulation law. Democratic Sen. Elizabeth Warren, who led the push against that Trump-era law, now wants to restore those rules on financial institutions. Biden is also calling on Congress to act.”

Five years ago, Warren was the most outspoken opponent of the Republican-led Congress’ push to undo regulations imposed under the 2010 Dodd-Frank law for small and midsize banks. The bill, led by Sen. Mike Crapo, R-Idaho, sought to reclassify the “too big to fail” standard, which came with enhanced regulatory scrutiny. By raising the threshold from $50 billion in assets to $250 billion, medium-size banks were exempted from those regulations.

“Had Congress and the Federal Reserve not rolled back the stricter oversight, S.V.B. and Signature would have been subject to stronger liquidity and capital requirements to withstand financial shocks,” Warren wrote Monday. “They would have been required to conduct regular stress tests to expose their vulnerabilities and shore up their businesses. But because those requirements were repealed, when an old-fashioned bank run hit S.V.B., the bank couldn’t withstand the pressure — and Signature’s collapse was close behind.”

Sen. Bernie Sanders, I-Vt., who also opposed the 2018 law, blamed it for Silicon Valley Bank’s collapse.

“Let’s be clear. The failure of Silicon Valley Bank is a direct result of an absurd 2018 bank deregulation bill signed by Donald Trump that I strongly opposed,” he said in a statement. “Five years ago, the Republican Director of the Congressional Budget Office released a report finding that this legislation would ‘increase the likelihood that a large financial firm with assets of between $100 billion and $250 billion would fail.’”

The 2018 battle featured intense lobbying by banks — including Silicon Valley Bank and an array of smaller community banks — that were seeking regulatory relief.

The bill passed the House 258-159, winning 225 Republicans and 33 Democrats. In the Senate, it needed some Democrats to defeat a filibuster and achieve 60 votes. Warren infuriated some colleagues when she called out some Senate Democrats by name for trying to weaken Dodd-Frank rules.

In the end, 17 Democrats joined a unanimous Senate Republican conference to pass it. Trump signed it into law.

The entire financial industry plays a role in the economy held by no other. The safekeeping role is why rules for bank deposits, the FDIC insurance mandates exist, and capitalization laws are in place. I think no one teaches about the Bank Holidays and Runs we experienced during the Great Depression. The more you chip away at what used to be legal differences and responsibilities between banks with deposits and fiduciary responsibility and their ability to play around with risky loans and investments, the more these things will reoccur. Also, speculative investors like hedge funds’ special tax treatment lower their risk costs and increase their ability to make investment decisions that have a likelihood of implosion. The rollback of substantial sections of Dodd-Frank was integral to last week’s runs.

https://twitter.com/ritujay/status/1634432765692366849

More importantly, the recent failures of financial institutions and companies involved with Cryptocurrencies will be part of the focus as state and federal regulators–including the Fed–do a post-mortem on both Silicon Valley and the Signature Bank in New York. These banks look like Country Clubs for risky and poorly managed loan portfolios. They have many big accounts backed up by cryptocurrency, a highly speculative and risky asset. This is from CNBC. “Regulators close crypto-focused Signature Bank, citing systemic risk.” The reporter is Yun Li.

The banking regulators said depositors at Signature Bank will have full access to their deposits, a move similar to that which was made to ensure depositors at the failed Silicon Valley Bank will get their money back.

“All depositors of this institution will be made whole. As with the resolution of Silicon Valley Bank, no losses will be borne by the taxpayer,” the regulators said.

The regulators shuttered Silicon Valley Bank on Friday and seized its deposits in the largest U.S. banking failure since the 2008 financial crisis — and the second-largest ever. The dramatic moves come just days after the tech-focused institution reported it was struggling, triggering a run on the bank’s deposits.

Signature is one of the main banks to the cryptocurrency industry, the biggest one next to Silvergate, which announced its impending liquidation last week. It had a market value of $4.4 billion as of Friday after a 40% sell-off this year, according to FactSet.

As of Dec. 31, Signature had $110.4 billion in total assets and $88.6 billion in total deposits, according to a securities filing.

To stem the damage and stave off a bigger crisis, the Fed and Treasury created an emergency program to backstop all deposits at both Signature Bank and Silicon Valley Bank using the Fed’s emergency lending authority.

The FDIC’s deposit insurance fund will be used to cover depositors, many of whom were uninsured due to the $250,000 cap on guaranteed deposits.

While depositors will have access to their money, equity and bondholders at both banks are being wiped out, a senior Treasury official said.

The article is written by DDay. “The Silicon Valley Bank Bailout Didn’t Need to Happen. The debate over protecting all deposits in a blink looks past the incompetence that got us here.” Buried in the fine print of the joint statement is something exciting. It states that “certain unsecured debtholders” and shareholders are not protected. Certain unsecured debtholders may likely apply to crypto-tainted accounts used to secure debt. The Fed has been anxious to get more involved with the rogue market. Will today’s Republican Congress let them?

The brightest minds in and around San Francisco Bay had an unadulterated meltdown over the weekend over the failure of Silicon Valley Bank. This was a failure that they themselves caused, mind you, engineering a digital flash bank run that forced SVB to realize heavy losses, mostly from interest rate hikes and the bank’s unbelievable failure to even attempt to manage interest rate risk.

The venture capitalist–led mob quickly moved on to another dire warning: Because over 90 percent of SVB’s depositors exceeded $250,000 in guaranteed FDIC insurance, the government must make them 100 percent whole, immediately, or every regional bank in America will see the same failure. Hedge fund titan Bill Ackman, venture capitalist David Sacks, and angel investor Jason Calacanis led the charge, saying that thousands of startup firms will have trouble making payroll, and other regionals won’t be able to stop a torrent of withdrawals. They essentially took out a match next to a gas pump and demanded that federal regulators not force them to light it.

It worked. Federal officials announced a backstop to “fully protect all depositors” at both Silicon Valley Bank and Signature Bank, which was also closed on Sunday. “Depositors will have access to all of their money starting Monday, March 13,” the joint announcement by Treasury, the Federal Reserve, and the FDIC read. A special bank assessment will offset losses, they say; all shareholders and bondholders “will not be protected,” with senior management fired. A $25 billion fund has been initiated to protect deposits, even though the theory is that no taxpayer funds will be implicated.

Run on San Antonio’s City-Central Bank and Trust Company during the Depression, 1931

Have I ever mentioned how much I’d admire California Representative Katie Porter?

THE FIRST WORDS OUT OF THE MOUTH of Rep. Katie Porter (D-CA) when I talked to her on Sunday were: “Can you believe we have to talk about this shit again?” She was referring to a conversation we had in 2018, when she was still just a financial expert and a candidate for Congress, about S.2155, which I call the Crapo bill, a reference to its co-author (Idaho Republican Sen. Mike Crapo) and its underlying contents.

Some of these provisions don’t mitigate risk; they encourage it. For depository institutions with fiduciary responsibilities, it’s like giving Bourbon-drenched pecan pie to alcoholics. Remember when Bill Gates sold Tesla short? Anyone with an excellent eye for financial statement analysis can see this stuff coming. But wait, how do you explain that “KPMG Gave SVB, Signature Bank Clean Bill of Health Weeks Before Collapse. Accounting firm faces scrutiny for audits of failed banks“? This is from Jonathan Weil and WSJ.

Silicon Valley Bank failed just 14 days after KPMG LLP gave the lender a clean bill of health. Signature Bank went down 11 days after the accounting firm signed off on its audit.

What KPMG knew about the two banks’ financial situation and what it missed will likely be the subject of regulatory scrutiny and lawsuits.

KPMG signed the audit report for Silicon Valley Bank’s parent, SVB Financial Group SIVB 0.00%increase; green up pointing triangle, on Feb. 24. Regulators seized the bank on March 10 after a surge of withdrawals threatened to leave it short of cash.

“Common sense tells you that an auditor issuing a clean report, a clean bill of health, on the 16th-largest bank in the United States that within two weeks fails without any warning, is trouble for the auditor,” said Lynn Turner, who was chief accountant of the Securities and Exchange Commission from 1998 to 2001.

Two crucial facts for determining whether KPMG missed the banks’ problems are when the bank runs began in earnest and when the bank’s management and KPMG’s auditors became aware of the crisis.

This reminds me of Moody’s, which had no idea how to rate tranches of mortgage-based swaps and completely missed the boat on the Mortgage crisis in 2008. You may also remember Moody’s role during the Junk Bond Kings’ rule in the late ’80s. This was also a time of intense deregulation of the industry.

. Moody’s also missed this current one. “Moody’s Failed to Warn About Silicon Valley Bank’s Problems. The prestigious rating agency still gave the bank of startups an A rating until its collapse on March 10, repeating the same errors of the subprime crisis in 2008.” This is from The Street and Luc Olinga.

Fifteen years after the subprime mortgage crisis which devastated the global economy, rating agencies continue to make the same mistakes.

At least, this seems to be the case with the prestigious rating agency Moody’s Investors Service.

Regulators shut down California’s Silicon Valley Bank on March 10, after its US Treasury bets went awry, due to the interest rate hike by the Federal Reserve.

Consequently, the Federal Deposit Insurance Corporation (FDIC) seized its assets and created a new entity, which will begin operating on March 13.

Created in 1983, Silicon Valley Bank, which presented itself as a “partner for the innovation economy,” offered higher interest rates on deposits than its larger rivals, to attract customers. The company then invested the clients’ money in long-dated Treasury bonds and mortgage bonds with strong returns.

Moody’s Gave Silicon Valley Bank an A Rating

This strategy had worked well in recent years. The bank’s deposits doubled to $102 billion at the end of 2020 from $49 billion in 2018. In 2021, deposits increased to $189.2 billion.

But everything turned upside down when the Federal Reserve began to raise interest rates, which made existing bonds held by SVB less valuable. As a result, the bank had to sell the bonds at a discount to cover withdrawals from its customers. In selling these bond positions, SVB had to take a significant loss of $1.8 billion.

Due to this loss, SVB suddenly announced that it needed to raise additional capital of $2.25 billion, by issuing new common and convertible preferred shares. This decision caused panic and a run on the bank.

While investors saw nothing coming, this is also the case with Moody’s Investors Service, whose role is to assess the intrinsic value of a company and its ability to meet its obligations, including its ability to pay lenders back. Rating agencies must flag the financial risks associated with a company.

But everything turned upside down when the Federal Reserve began to raise interest rates, which made existing bonds held by SVB less valuable. As a result, the bank had to sell the bonds at a discount to cover withdrawals from its customers. In selling these bond positions, SVB had to take a significant loss of $1.8 billion.

Due to this loss, SVB suddenly announced that it needed to raise additional capital of $2.25 billion, by issuing new common and convertible preferred shares. This decision caused panic and a run on the bank.

While investors saw nothing coming, this is also the case with Moody’s Investors Service, whose role is to assess the intrinsic value of a company and its ability to meet its obligations, including its ability to pay lenders back. Rating agencies must flag the financial risks associated with a company.

American Union Bank, New York City. April 26, 1932.

I’ve lived through a banking crisis in charge of strategic planning and financial statement forecasting for one of the original too big to fail Savings and Loan Companies in the early 1980s. I was also trying to hedge our loan commitments using GNMA futures which is why Derivatives are real to me. Any time interest rates start moving in the wrong direction and any bank that hasn’t realigned their related risks, like being long on one side of the balance sheet and short on the other, you’ll lose big.

I had to tell the head of Financial Operations there was no way to break even when every rate marks an asset to market with every tick, and you’re mismatched. I was barely 25 at the time. I also saw loan brokers selling mortgages where due diligence was lacking in 2005. A student told me he was being offered a mortgage based on his student loan as income. I can’t imagine any in-house loan officer being that ignorant. That’s what happens when you farm out your core business ou to salespeople earning money by volume. I can’t imagine how Moody’s or major Auditing firms keep missing this. They’re probably as captured by their customers as the politicians are captured by their lobbyists and checks. Right Senator Sinema?

James Stewart and Donna Reed in a scene from the film ‘It’s A Wonderful Life’, 1946. (Photo by RKO Radio Picture/Getty Images)

So, these bank runs don’t exactly look like the ones in those black-and-white photographs from the 1930s. This is a good explanation from Fast Company. What exactly is a Digital Flash Bank Run? It’s not a DC comic. Silicon Valley Bank: An ‘It’s a Wonderful Life’ bank run for the digital age. The downfall of the Valley institution, which has been called “the backbone of the startup economy,” was caused by a good old-fashioned bank run, but one that ran at internet speed.”

The run began on Thursday, after a powerful Silicon Valley VC—Peter Thiel’s Founders Fund—had begun advising its portfolio companies to withdraw their money from SVB, sources told Fast Company. Other VCs soon caught wind of the advisory and began advising their own portfolio companies to withdraw funds from SVB, the people said. As the withdrawals accelerated, the bank began taking steps to stem the tide and preserve its solvency—just like George Bailey did in the 1946 classic It’s a Wonderful Life.

SVB Financial Group CEO Greg Becker seemed to be reading from director Frank Capra’s script when he uttered the fateful words “stay calm” during a Thursday conference call with customers, as fears over the bank’s solvency grew. Those words probably only increased depositors’ anxieties. And the withdrawals likely continued to snowball.

“The whole thing was predicated on a few folks who put out calls to make withdrawals,” Spencer Greene, a general partner at the venture fund TSVC, tells Fast Company. “I think the folks who made those calls weren’t correct on the facts, but once the thing got going it was hard to stop.” In other words, before the run started there was not sufficient evidence to suggest the bank was facing serious solvency issues.

Northern Rock Bank run, September 2007

Just another point, we knew these things could happen. Here’s a 2019 article speculating about a digital bank flash run by Joe McGrath, writing for The Raconteur. “Turmoil, panic and bank runs in a digital future.”

Potentially, cash can now be transferred from accounts in greater amounts, more quickly than before and, even if banks enforce temporary limits on online withdrawals, what effect would the resulting panic have on the banking system as a whole?

“In a world without physical cash, the rules of engagement for situations such as a bank run will require a different framework,” says Simon Fairbairn, director of solution development, western Europe, for Ingenico Group. “The rules and systems of today will need to evolve to accommodate the demands of a run.”

Mr Fairbairn questions whether present digital banking infrastructure is sufficient to cope with sustained pressure of this nature. “Regulation, compliance, technology; processes have all evolved to try and prevent the sins of the past, but until tested, can we really be sure it won’t already be found wanting,” he says.

It may sound like scaremongering, but Mr Fairbairn’s cautious view has broad support from many in the financial services community.

“A digital bank run in a hypothetical future would be much more dangerous as it would happen in seconds and minutes when clients could simply use mobile banking apps to transfer money to another account,” says Susanne Chishti, chief executive of Fintech Circle.

“Such a digital bank run would be much more difficult to contain and an appropriate technical response for such a scenario would have to be coded in at the outset to offer any chance of being effective.”

In 2020, Harvest Finance experienced the first type of digital bank run. “Harvest Finance: $24M Attack Triggers $570M ‘Bank Run’ in Latest DeFi Exploit, Harvest Finance has seen its total value locked drop by more than $500 million in the 12 hours since being hit by a flash loan attack.” DeFi is short for Decentralized Finance, which is based on peer-to-peer finance services on blockchains. Welcome to the Wild West World of cryptocurrency and bitcoins. This should give you pause.

An arbitrage trade exploiting weak points in decentralized finance (DeFi) protocol Harvest Finance led to some $24 million in stablecoins being siphoned away from the project’s pools on Monday, according to CoinGecko.

According to reports, an attacker used a flash loan – a technique that allows a trader to take on massive leverage without any downside – to manipulate DeFi prices for profit. The exploit sent the platform’s native token, FARM, tumbling by 65% in less than an hour, followed by the project’s total value locked (TVL), which dropped from over $1 billion before the exploit to $430 million as of press time.

The funds were eventually swapped for bitcoin (BTC), but not before being swept through Ethereum mixing service Tornado Cash.

The jargon term for this was a “bad harvest.” Stay out of this stuff is the only thing I have to say, which is the advice I would have given to these banks. Unfortunately, Silicon Valley is rife with Elon Musk Clones taking risks for adventure and attention. All traders have their own language. I’m still surprised youngest daughter can keep her department of derivatives traders and products on a leash. They’ve always thought of themselves as Wild West Cowboys. (See Lions of Wall Street.) But then, she and the brokerage firms she’s worked for are licensed and babysat by the SEC to keep the nonsense in check. We both stay out of this market.

So, a part of this and a bit more will be a lecture for me tomorrow. Last year the Game Stop thing did this to me. You’ll be glad to know billionaire Carl Icahn is happy about that crash. Someone always is because there are two sides to every trade. If you’re head’s spinning, you’re doing just fine. I got a Ph.D. and real-life experience in the stuff, plus a daughter that lives it daily and who I consult for a reality check. It still makes my head spin.

What’s on your reading and blogging list today?

And the SEC is far behind

Down in the swamp with the gators and flamingos

A long way from Liechtenstein

I’m a junk bond king playing Seminole Bingo

And my Wall Street wiles

Don’t help me even slightly

‘Cause I never have the numbers

And I’m losing nightly

I cashed in the last of my Triple B bonds

Got a double-wide on the Tamiami Trail

I parked it right outside the reservation

Fifteen minutes from the Collier County Jail

(Warren Zevon, backed up by Neil Young live)

Bernanke nudges the Do Nothing Congress

Posted: November 2, 2011 Filed under: Economy, U.S. Economy | Tags: Federal Reserve Bank, FOMC. Ben Bernanke 10 Comments It’s been interesting watching Bernanke get more shrill with each post FOMC meeting news conference. First, he points out that the right wing meme about the unemployment being structural is wrong headed. He talks about why it’s important to respond to cyclical unemployment. This is something congress has being ignoring while doing important things like passing bills to ensure that trust in imaginary friends is printed on money.

It’s been interesting watching Bernanke get more shrill with each post FOMC meeting news conference. First, he points out that the right wing meme about the unemployment being structural is wrong headed. He talks about why it’s important to respond to cyclical unemployment. This is something congress has being ignoring while doing important things like passing bills to ensure that trust in imaginary friends is printed on money.

“We believe that a good bit of the unemployment were are seeing is what economists would call cyclical unemployment, that is unemployment arising because of inadequate demand in the economy. If that is the case, then monetary policy by lowering interest rates, making financial conditions more accommodative, should stimulate demand, stimulate spending and over a period of time that should help bring cyclical unemployment down. It’s also possible that some of the increase in unemployment reflects so-called structural factors, mismatches between worker skills and job opportunities, loss of skills, geographical location, etc. If that’s the case then monetary policy is much less effective because only other kinds of labor market policies can make progress against that type of unemployment. But again I do think that a considerable part of the unemployment that we are seeing is cyclical. Final comment, cyclical unemployment left untreated, so to speak, for a long time can become structural unemployment as people lose skills, they lose attachment to the labor force.”

He also asked for a little help from congress. Bernanke basically tired to ask for stimulus without using the word since the Congress has branded it anathema.

“With respect to the current economy we are currently continuing our accommodative monetary policy. We are trying to do our best to support economic growth and job creation. It would be helpful if we could get assistance from some other parts of the government to work with us to help create more jobs. But certainly we are doing our part to create more jobs, more opportunities in America.”

Sorry, Ben, the “other parts of government” are just to busy to help the economy work. They prefer to posture and preen. Bernanke has amped up the volume as pointed out at Political Animal. Kevin Drum thinks that the next presser will be when Bernanke says “Will you guys stop griping about the damn budget, get off your butts, and build a few effin bridges instead? Jesus.”

Saturday Reads: Dr. Martin Luther King’s Dreams, Waiting for Irene, and Bernanke’s Complaint

Posted: August 27, 2011 Filed under: Barack Obama, Civil Rights, Domestic Policy, Economy, jobs, morning reads, poverty, U.S. Economy, U.S. Politics | Tags: Barack Obama, Ben Bernanke, Cornel West, Federal Reserve Bank, Hurrican Irene, I Have A Dream speech, leadership vacuum, Martin Luther King, media frenzy, oligarchy, revolution 63 Comments

By Mr. Fish, Truthdig.org

Good Morning! We are approaching the 48th anniversary of the March on Washington for Jobs and Freedom (remember those?) and Martin Luther King’s “I have a dream” speech. Perhaps it is fitting that the ceremony to be held tomorrow to commemorate the anniversary has been postponed indefinitely. After all, King’s dream of ending poverty in American has certainly been postponed indefinitely. Ironically, we now have a “Black President” who as different from Dr. King as night from day. Oh, if only King were here today to speak truth to this sorry excuse for a President!

A reminder from the Center for American Progress: Dr. King’s Legacy Relevant in Today’s Budget Battles

In the 1960s, Americans had a government that refused to deliver basic human rights to its people. Over time, after battles in the courts and the political arena, laws such as the Civil Rights Act of 1964 and the Equal Employment Opportunity Act of 1972 were passed. But despite these great accomplishments the fight continued because many Americans of all racial backgrounds were still living below the poverty line.

So in 1967, Dr. King and the Southern Christian Leadership Conference decided to organize and lead the Poor People’s Campaign to combat poverty. The goal was to push Congress to create an “Economic Bill of Rights” that would establish how the federal government would address and solve the country’s poverty issues. It called for full employment, affordable housing, reasonable living wages, and equitable education opportunities for the poor. Momentum built up around the country, but unfortunately the campaign ended early due to the tragic assassination of Dr. King and lack of organization to continue the efforts.

Cornel West had a very appropriate op-ed in the NYT a couple of days ago: Dr. King Weeps From His Grave Here is a relevant excerpt:

The age of Obama has fallen tragically short of fulfilling King’s prophetic legacy. Instead of articulating a radical democratic vision and fighting for homeowners, workers and poor people in the form of mortgage relief, jobs and investment in education, infrastructure and housing, the administration gave us bailouts for banks, record profits for Wall Street and giant budget cuts on the backs of the vulnerable.

As the talk show host Tavis Smiley and I have said in our national tour against poverty, the recent budget deal is only the latest phase of a 30-year, top-down, one-sided war against the poor and working people in the name of a morally bankrupt policy of deregulating markets, lowering taxes and cutting spending for those already socially neglected and economically abandoned. Our two main political parties, each beholden to big money, offer merely alternative versions of oligarchic rule.

The absence of a King-worthy narrative to reinvigorate poor and working people has enabled right-wing populists to seize the moment with credible claims about government corruption and ridiculous claims about tax cuts’ stimulating growth. This right-wing threat is a catastrophic response to King’s four catastrophes; its agenda would lead to hellish conditions for most Americans.

King weeps from his grave. He never confused substance with symbolism. He never conflated a flesh and blood sacrifice with a stone and mortar edifice. We rightly celebrate his substance and sacrifice because he loved us all so deeply. Let us not remain satisfied with symbolism because we too often fear the challenge he embraced. Our greatest writer, Herman Melville, who spent his life in love with America even as he was our most fierce critic of the myth of American exceptionalism, noted, “Truth uncompromisingly told will always have its ragged edges; hence the conclusion of such a narration is apt to be less finished than an architectural finial.”

King’s response to our crisis can be put in one word: revolution. A revolution in our priorities, a re-evaluation of our values, a reinvigoration of our public life and a fundamental transformation of our way of thinking and living that promotes a transfer of power from oligarchs and plutocrats to everyday people and ordinary citizens.

Yes we need a revolution. We desperately need to revise our priorities and values and to end the transfer of wealth and power from the people to the oligarchs. Who will lead that revolution? We have never been more in need of strong, honest, caring leaders and yet we have a complete vacuum of leadership. What is to become of our country?

Of course Hurricane Irene is the more immediate focus and the object of the media sharks’ feeding frenzy for today. Nothing so pedestrian as putting people back to work or ending poverty could interest them. Interestingly, big media seems to be ignoring the fact that the hurricane has weakened significantly and that the eye has collapsed, meaning that there is unlikely to be any more intensification of the storm. I suppose it could still do quite a bit of damage along the coastline, but as a Bostonian I’ve seen so many of these huge storms fail to live up to the hype that I’m skeptical of this one. I hope I’m right this time.

Jeff Masters at Weather Underground yesterday:

Satellite data and measurements from the Hurricane Hunters show that Irene is weakening. A 9:21 am EDT center fix by an Air Force Reserve aircraft found that Irene’s eyewall had collapsed, and the central pressure had risen to 946 mb from a low of 942 mb this morning. The highest winds measured at their flight level of 10,000 feet were 125 mph, which would normally support classifying Irene as a Category 3 hurricane with 115 mph winds. However, these winds were not mixing down to the surface in the way we typically see with hurricanes, and the strongest surface winds seen by the aircraft with their SFMR instrument were just 90 mph in the storm’s northeast eyewall. Assuming the aircraft missed sampling the strongest winds of the hurricane, it’s a good guess that Irene is a mid-strength Category 2 hurricane with 100 mph winds. Satellite imagery shows a distinctly lopsided appearance to Irene’s cloud pattern, with not much heavy thunderstorm activity on the southwest side. This is due to moderate wind shear of 10 – 20 knots due to upper-level winds out of the southwest. This shear is disrupting Irene’s circulation and has cut off upper-level outflow along the south side of the hurricane. No eye is visible in satellite loops, but the storm’s size is certainly impressive. Long range radar out of Wlimington, North Carolina, shows that the outermost spiral bands from Irene are now beginning to come ashore along the South Carolina/North Carolina border. Winds at buoy 41004 100 miles offshore from Charleston, SC increased to 36 mph as of 10 am, with significant wave heights of 18 feet.

And from last night: “Irene continues to weaken.”

Satellite data and measurements from the Hurricane Hunters show that Irene continues to weaken. A 1:32 pm EDT center fix by an Air Force Reserve aircraft found that Irene’s eyewall is still gone, and the central pressure had risen to 951 mb from a low of 942 mb this morning. The winds measured in Irene near the surface support classifying it as a strong Category 1 hurricane or weak Category 2. Satellite imagery shows a distinctly lopsided appearance to Irene’s cloud pattern, with not much heavy thunderstorm activity on the southwest side. This is due to moderate southwesterly wind shear of 10 – 20 knots. This shear is disrupting Irene’s circulation and has cut off upper-level outflow along the south side of the hurricane. No eye is visible in satellite loops, but the storm’s size is certainly impressive. Long range radar out of Wilmington, North Carolina, shows that the outermost spiral bands from Irene have moved ashore over North Carolina. Winds at buoy 41004 100 miles offshore from Charleston, SC increased to 47 mph, gusting to 60 mph at 3 pm EDT, with significant wave heights of 25 feet.

New York City has ordered 250,000 people to evacuate from coastal areas.

New York City officials issued what they called an unprecedented order on Friday for the evacuation of about 250,000 residents of low-lying areas at the city’s edges — from the expensive apartments in Battery Park City to the roller coaster in Coney Island to the dilapidated boardwalk in the Rockaways — warning that Hurricane Irene was such a threat that people living there simply had to get out.

Officials made what they said was another first-of-its kind decision, announcing plans to shut down the city’s entire transit system on Saturday — all 468 subway stations and 840 miles of tracks, and the rest of nation’s largest mass transit network: thousands of buses in the city, as well as the buses and commuter trains that reach from Midtown Manhattan to the suburbs.

Underscoring what Mayor Michael R. Bloomberg and other officials said was the seriousness of the threat, President Obama approved a request from Gov. Andrew M. Cuomo of New York to declare a federal emergency in the state while the hurricane was still several hundred miles away, churning toward the Carolinas. The city was part of a hurricane warning that took in hundreds of miles of coastline, from Sandy Hook, N.J., to Sagamore Beach, Mass.

From what I’ve heard, the Jersey Shore may get hit worse than NYC, but who knows? I know we have a few commenters from NJ, so I hope they will keep us updated on the situation there. In Boston, they are getting warnings about the storm surges for people along the coast and the Cape and islands.

BOSTON — As Hurricane Irene began to batter the Carolina Coast on Friday afternoon, a hurricane warning was issued for Cape Cod, Martha’s Vineyard, New York City and coastal Connecticut.

A tropical storm warning was issued for the North and South shores, and a tropical storm watch was issued for areas of southern New England further inland….

Massachusetts Gov. Deval Patrick declared a state of emergency ahead of the storm. He said he is particularly concerned because Irene will likely take a path through central Massachusetts, with fierce, damage-causing winds and storm surges on the eastern, coastal side of the state, and at least 10 inches of heavy rain leading to flooding to the west.

Here’s a little comic relief. Some ESPN guy (a former golfer) got in trouble for mocking President Obama on Twitter (has the First Amendment been repealed or what?)

ESPN is coming down on Paul Azinger for mocking President Obama on Twitter. The golf analyst tweeted Thursday the commander in chief plays more golf than he does — and that Azinger has created more jobs this month than Obama has.

On Friday ESPN ‘reminded” Azinger his venture into political punditry violates the company’s updated social network policy for on-air talent and reporters.

“Paul’s tweet was not consistent with our social media policy, and he has been reminded that political commentary is best left to those in that field,” spokesman Andy Hall told Game On! in a statement.

ESPN’s Hall would not comment on whether Azinger, who won the 1993 PGA Championship, will be fired, suspended or punished in some way. “We handle that internally,” he said.

In economics news, Ben Bernanke gave his eagerly anticipated speech yesterday, and basically said that the politicians have screwed up the economy and he hopes they won’t completely sink it with their insanely stupid policies based on Reagan era fantasies. If you’re interested, here are a few links to reactions to Bernanke’s speech.

Derek Thompson at The Atlantic: Bernanke: The Debt Ceiling Debate Nearly Broke the Recovery

Andrew Leonard at Salon: Bernanke Declines to Commit Treason

Jenine Aversa at Bloomberg: Bernanke Scholar Advises Bernanke Fed Chief to Be Bold on Monetary Policy

Those are my reading recommendations for today. What are you reading and blogging about?

US Financial Regulation and Arbitrage

Posted: January 5, 2011 Filed under: Bailout Blues, commercial banking, Corporate Crime, Equity Markets, financial institutions, Global Financial Crisis, investment banking, Team Obama, U.S. Economy | Tags: Federal Reserve Bank, financial regulation, Obama Financial Reform, OCC, Regulatory Arbitrage, SEC 17 CommentsThere is no doubt that we have had a major world wide financial collapse drastically affecting many innocent people in terms of livelihood and life long savings. It is fair to say that if the regulators had done their job, the country would have not had the hard landing that was experienced in 2008. The 2010 Financial Reform Bill kicked the can down to the Regulators for implementation and the bankers still have influence. This article takes a look at who the regulators were and how they did or did not do their job. The Obama people in the regulator domain are identified along with examples of Bush regulator failures. Hopefully this will give insight into what is being done to preclude another crisis

The financial industry has a gaggle of regulators, each with its politically protected turf.

From Wikopedia: Financial regulation is a form of regulation or supervision, which subjects financial institutions to certain requirements, restrictions and guidelines, aiming to maintain the integrity of the financial system.

Regulation is an unnecessarily a complex subject. It is important to understand that in some cases financial entities can choose their regulator. Some regulators were much more lenient and in many cases banks switched to them, hence the term Regulatory Arbitrage. The following are the major Federal regulators: FED, SEC, OCC, OTS, FDIC, CFTC  and FINRA described below. Except for the FED, most of these organizations have direct or indirect ties to the Treasury organization.

and FINRA described below. Except for the FED, most of these organizations have direct or indirect ties to the Treasury organization.

FED – Federal Reserve System

From Wikopedia: Its duties today, according to official Federal Reserve documentation, are to conduct the nation’s monetary policy, supervise and regulate banking institutions, maintain the stability of the financial system and provide financial services to depository institutions, the U.S. government, and foreign official institutions.Current chairman is Ben Bernanke, the former chairman was Alan Greenspan. Much more on Mr Greenspan later.

SEC – Securities and Exchange Commission

From Wikopedia: It holds primary responsibility for enforcing the federal securities laws and regulating the securities industry, the nation’s stock and options exchanges, and other electronic securities markets in the United States. Mary Schapiro is the current Chair. Predesessors were; Christopher Cox – 2005-2009, William H. Donaldson – 2003-2005, Harvey Pitt – 2001-03

OCC – Office of Comptroller of the Currency

From Wikopedia: US federal agency established by the National Currency Act of 1863 and serves to charter, regulate, and supervise all national banks and the federal branches and agencies of foreign banks in the United States. Current Acting Chairman is John Walsh. Previous Chairman were John C. Dugan – (2005 – 2010) John D. Hawke, Jr. – (1998–2004)

OTS – Office of Thrift Supervision ( recently folded into OCC)

From Wikopedia: United States federal agency under the Department of the Treasury. It was created in 1989 as a renamed version of another federal agency (that was faulted for its role in the Savings and loan crisis). Like other US federal bank regulators, it is paid by the banks it regulates. The OTS was initially seen as an aggressive regulator, but was later lax. Declining revenues and staff led the OTS to market itself to companies as a lax regulator in order to get revenue.

FDIC – Federal Deposit Insurance Corporation

From Wikopedia: United States government corporation created by the Glass-Steagall Act of 1933. It provides deposit insurance, which guarantees the safety of deposits in member banks, currently up to $250,000 per depositor per bank. The FDIC insures deposits at 7,895 institutions. The FDIC also examines and supervises certain financial institutions for safety and soundness, performs certain consumer-protection functions, and manages banks in receiverships (failed banks).

Sheila Bair is the current chairman of the FDIC and is viewed as a serious regulator with the right incentives for all concerned.

CFTC – Commodity Futures Trading Commission

From Wikopedia: The stated mission of the CFTC is to protect market users and the public from fraud, manipulation, and abusive practices related to the sale of commodity and financial futures and options, and to foster open, competitive, and financially sound futures and option markets.

CFTC is considered to be the primary regulator for Credit Default Swaps in the Dodd Frank regulation scheme.

FINRA – Financial Industry Regulatory Authority

From Wikopedia: In the United States, the Financial Industry Regulatory Authority, Inc., or FINRA, is a private corporation that acts as a self-regulatory organization (SRO). FINRA is the successor to the National Association of Securities Dealers, Inc. (NASD). Though sometimes mistaken for a government agency, it is a non-governmental organization that performs financial regulation of member brokerage firms and exchange markets.

Previously run by Mary Shapiro, FINRA has been critisized as being a ineffective regulator. Most notable was their (and SEC) allowing Bernie Madow to continue for 10 years to operate despite being warned by a whistle blower. When testifying before congress, the whistle blower (Harry Markopolos) said SEC was incompetent, FINRA was corrupt.

It must be said that Financial Regulation in the United States is done by committee of political bureauocrats. It is important to be aware of the fact that many of them are funded by fee’s assessed to the agencies they regulate. So opportunity for Regulatory Capture and Regulatory Arbitrage is prevalent in these agencies. The clear example is Office of Thrift Supervision bowing to their clients. The opposite example is that of Sheila Bair who tries to do the right thing for her clients despite critisizm.

Recent Comments