Posted: May 24, 2014 | Author: bostonboomer | Filed under: Gun Control, income inequality, morning reads, racism, The Bonus Class, U.S. Economy, U.S. Politics | Tags: Chris Giles, Donald Sterling, economic theory, Financial Times., guns, inequality, Kevin Drum, LA Clippers, mass murder, mass shootings, NBA, offshore tax havens, open carry laws, Paul Krugman, Reinhart and Rogoff, Shelly Sterling, Ta-Nehisi Coates, The Case for Reparations, The Economist, Thomas Picketty, wealth distribution, wealth vs. income |

Thomas Picketty

Have a Stupendous Saturday!

It’s too bad Dakinikat is so busy today, because there’s an economics food fight brewing. Perhaps she’ll still find time to comment on the controversy later the evening after she returns home with her newly adopted canine family member, Temple. Meanwhile, I’ll do my best to describe the dispute over Thomas Picketty’s conclusions about wealth inequality, published in his book Capital in the Twenty-first Century.

The Accusations:

At the Financial Times, Economics Editor Chris Giles has claims to have found problems with Picketty’s work: Piketty findings undercut by errors.

Thomas Piketty’s book, ‘Capital in the Twenty-First Century’, has been the publishing sensation of the year. Its thesis of rising inequality tapped into the zeitgeist and electrified the post-financial crisis public policy debate.

But, according to a Financial Times investigation, the rock-star French economist appears to have got his sums wrong.

The data underpinning Professor Piketty’s 577-page tome, which has dominated best-seller lists in recent weeks, contain a series of errors that skew his findings. The FT found mistakes and unexplained entries in his spreadsheets, similar to those which last year undermined the work on public debt and growth of Carmen Reinhart and Kenneth Rogoff.

The central theme of Prof Piketty’s work is that wealth inequalities are heading back up to levels last seen before the first world war. The investigation undercuts this claim, indicating there is little evidence in Prof Piketty’s original sources to bear out the thesis that an increasing share of total wealth is held by the richest few.

Prof Piketty, 43, provides detailed sourcing for his estimates of wealth inequality in Europe and the US over the past 200 years. In his spreadsheets, however, there are transcription errors from the original sources and incorrect formulas. It also appears that some of the data are cherry-picked or constructed without an original source.

John Maynard Keynes

In one specific example, Giles says the corrected data do not show significant growth in Europe since 1970. In a second article, Giles goes into more detail. In addition, he argues that the U.S. data doesn’t support the conclusion that a greater proportion of the wealth is controlled by top 1% than in recent decades. He does admit to the top 10% controlling a greater share of wealth than previously.

An investigation by the Financial Times, however, has revealed many unexplained data entries and errors in the figures underlying some of the book’s key charts.

These are sufficiently serious to undermine Prof Piketty’s claim that the share of wealth owned by the richest in society has been rising and “the reason why wealth today is not as unequally distributed as in the past is simply that not enough time has passed since 1945”.

After referring back to the original data sources, the investigation found numerous mistakes in Prof Piketty’s work: simple fat-finger errors of transcription; suboptimal averaging techniques; multiple unexplained adjustments to the numbers; data entries with no sourcing, unexplained use of different time periods and inconsistent uses of source data….

A second class of problems relates to unexplained alterations of the original source data. Prof Piketty adjusts his own French data on wealth inequality at death to obtain inequality among the living. However, he used a larger adjustment scale for 1910 than for all the other years, without explaining why.

In the UK data, instead of using his source for the wealth of the top 10 per cent population during the 19th century, Prof Piketty inexplicably adds 26 percentage points to the wealth share of the top 1 per cent for 1870 and 28 percentage points for 1810.

A third problem is that when averaging different countries to estimate wealth in Europe, Prof Piketty gives the same weight to Sweden as to France and the UK – even though it only has one-seventh of the population.

Get even more detail and charts here: Data problems with Capital in the 21st Century.

Karl Marx

The Pushback So Far:

Paul Krugman: Is Piketty All Wrong?

Great buzz in the blogosphere over Chris Giles’s attack on Thomas Piketty’s Capital in the 21st Century. Giles finds a few clear errors, although they don’t seem to matter much; more important, he questions some of the assumptions and imputations Piketty uses to deal with gaps in the data and the way he switches sources. Neil Irwin and Justin Wolfers have good discussions of the complaints; Piketty will have to answer these questions in detail, and we’ll see how well he does it.

Krugman suggests that Giles may be doing something wrong.

I don’t know the European evidence too well, but the notion of stable wealth concentration in the United States is at odds with many sources of evidence. Take, for example, the landmark CBO study on the distribution of income; it shows the distribution of income by type, and capital income has become much more concentrated over time:

It’s just not plausible that this increase in the concentration of income from capital doesn’t reflect a more or less comparable increase in the concentration of capital itself….

And there’s also the economic story. In the United States, income inequality has soared since 1980 by any measure you use. Unless the affluent starting saving less than the working class, this rise in income disparity must have led to a rise in wealth disparity over time.

At Mother Jones, Kevin Drum notes that

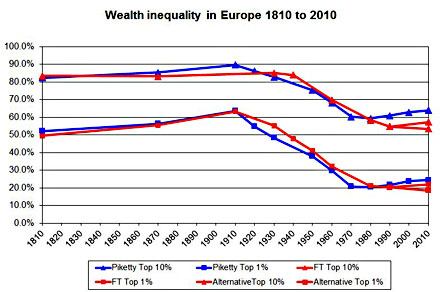

Giles’ objections are mostly to the data regarding increases in wealth inequality over the past few decades, and the funny thing is that even Piketty never claims that this has changed dramatically. The end result of Giles’ re-analysis of Piketty’s data is [below] with Piketty in blue and Giles in red. As you can see, Piketty estimates a very small increase since 1970.

R.A. at The Economist: A Piketty problem?

Milton Friedman

Mr Giles’s analysis is impressive, and one certainly hopes that further work by Mr Giles, Mr Piketty or others will clarify whether mistakes have been made, how they came to be introduced and what their effects are. Based on the information Mr Giles has provided so far, however, the analysis does not seem to support many of the allegations made by the FT, or the conclusion that the book’s argument is wrong.

There are four important questions raised by the FT‘s work. First, which data are wrong? Second, how did errors in the work, if they are errors, come to be introduced? Third, how do the errors affect the specific points made in the relevant chapters? And fourth, how do the errors affect the fundamental conclusions of the book?

Mr Giles focuses on wealth inequality, to which Mr Piketty turns in Chapter 10 of his book. Mr Piketty has not published nearly as much research on the question of wealth inequality, and it seems that much of the analysis in Chapter 10 was done specifically for the book, based on others’ research. Mr Piketty’s wealth-inequality analysis certainly matters as a component of the book’s argument, but it is not accurate to say, as Mr Giles does, that the results in Chapter 10 constitute the “central theme” of the book.

Are the data wrong? Mr Giles identifies discrepancies between source material cited by Mr Piketty and the figures that appear in the book. He identifies cases in which Mr Piketty appears to have chosen to use data from one source when another would have made more sense. Further, the calculations in Mr Piketty’s spreadsheets (which have been available online since the book’s publication) seem to include adjustments in the data that are not adequately explained, and some figures for which Mr Giles cannot find a documented source. Finally, Mr Piketty has made choices concerning weighting of data used in averages, and assigning of data from one year (1935, for example) to another (1930) when such assignments seem unnecessary or inadvisable.

Alan Greenspan

The author concludes that, unfortunately, ideology will determine how many people respond to the Giles critique. Much more extensive analysis at the link.

Here is Picketty’s–presumably preliminary–response to Giles in a letter to the Financial Times:

Let me also say that I certainly agree that available data sources on wealth are much less systematic than for income. In fact, one of the main reasons why I am in favor of wealth taxation and automatic exchange of bank information is that this would be a way to develop more financial transparency and more reliable sources of information on wealth dynamics (even if the tax was charged at very low rates, which you might agree with).

For the time being, we have to do with what we have, that is, a very diverse and heterogeneous set of data sources on wealth: historical inheritance declarations and estate tax statistics, scarce property and wealth tax data, and household surveys with self-reported data on wealth (with typically a lot of under-reporting at the top). As I make clear in the book, in the on-line appendix, and in the many technical papers I have published on this topic, one needs to make a number of adjustments to the raw data sources so as to make them more homogenous over time and across countries. I have tried in the context of this book to make the most justified choices and arbitrages about data sources and adjustments. I have no doubt that my historical data series can be improved and will be improved in the future (this is why I put everything on line). In fact, the “World Top Incomes Database” (WTID) is set to become a “World Wealth and Income Database” in the coming years, and we will put on-line updated estimates covering more countries. But I would be very surprised if any of the substantive conclusion about the long run evolution of wealth distributions was much affected by these improvements.

I thought this was important:

…my estimates on wealth concentration do not fully take into account offshore wealth, and are likely to err on the low side. I am certainly not trying to make the picture look darker than it it. As I make clear in chapter 12 of my book (see in particular table 12.1-12.2), top wealth holders have apparently been rising a lot faster average wealth in recent decades, at least according to the wealth rankings published in magazines such as Forbes. This is true not only in the US, but also in Britain and at the global level (see attached table). This is not well taken into account by wealth surveys and official statistics, including the recent statistics that were published for Britain. Of course, as I make clear in my book, wealth rankings published by magazines are far from being a perfectly reliable data source. But for the time being, this is what we have, and what we have suggests that the concentration of wealth at the top is rising pretty much everywhere.

In Other News:

There has been a mass shooting in Southern California–this time perpetrated from behind the wheel of a car. From the LA Times, 7 dead in drive-by shooting near UC Santa Barbara.

The shootings began about 9:30 p.m., a sheriff’s spokeswoman told KEYT-TV. It wasn’t clear what the attacker’s motivation might have been.

An 18-year-old Newport Beach man who was visiting Santa Barbara described a confusing scene as the shots rang out.

Nikolaus Becker was eating outside The Habit, 888 Embarcadero Del Norte, near the scene when the first set of shots was fired about 9:30 p.m. At first he thought it was firecrackers. A group of three to five police officers who were nearby started to casually walk toward the sounds, said Becker, but ran when a second round of shots broke out.

“That’s when they yelled at us to get inside and take cover,” Becker said.

The BMW took a sharp turn in front of The Habit, Becker said, and moments later a third round of shots was heard. Becker and his friends moved toward the restaurant’s kitchen but were told to wait in the seating area by employees.

He estimates there were at least 13 to 15 shots total at three locations. The locations were about 100 yards from one another.

The shooter, whose motivation is unknown, was found dead in his BMW. It’s not yet clear if he shot himself or was killed by sheriff’s deputies.

In another gun-related story, TPM reports that some gun nuts are reconsidering their campaign of carrying long guns into public places: Scaring The Crap Out of People Oddly Not Winning Fans.

Earlier this week we reported how Chipotle felt obliged to ask its customers not to bring guns to chipotle restaurants. Seems like a reasonably enough request to most of us. And it’s been preceded by similar requests by various other chains like Starbucks and others.

Now the top pro-gun group in Texas pushing the demand for “open carry” firearm rights and trying to get people to show up at various restaurant chains with long guns is deciding it may not be such a hot idea after all.

Open Carry Texas and a group of other aggressive gun rights groups have issued a joint statement telling their members, Dudes, let’s stop taking our guns to restaurants. It’s freaking people out and making them hate us.

Read the full statement at TPM.

Soon-to-be former LA Clippers owner Donald Sterling has signed over the team to his wife and wants her to negotiate the sale.

Shelly Sterling, who previously shared ownership of the beleaguered NBA franchise with her estranged husband, is now in talks with the NBA over selling the team, the source said.

The NBA banned Donald Sterling for life from all league events after an audio tape became public that caught him on tape uttering racist comments to his assistant V. Stiviano. He told her not to post photos of herself with black people on Instagram — such as Magic Johnson — or bring them to his basketball games.

But the NBA isn’t buying it. From ESPN: Why the NBA won’t allow Shelly Sterling to control the Clippers.

At first glance, Donald Sterling’s gesture may seem like serendipitous news for the NBA. Taking him at his word, Donald Sterling has agreed to leave the league without a fight and has signed off on the sale of his team. Digging deeper, however, reveals possible ulterior motives on Sterling’s part to delay and potentially block the sale of the team. Do not forget a crucial point: capital gain taxes. As first reported by SI.com, the Sterlings have significant incentives under capital gain tax law to avoid the sale of the team and keep it in the Sterling family. Doing so, would save them hundreds of millions of dollars. Also, contrary to some reports, the Sterlings are unlikely to benefit from the “involuntary conversion” tax avoidance provision of the Internal Revenue Code. The bottom line is if the Sterlings have to sell the Clippers, they will probably pay hundreds of millions in state and federal taxes.

Along those lines, Donald Sterling’s proposed maneuver does not accomplish the NBA’s goal of ousting the entire Sterling family on June 3. As explained in a previous SI.com article, the NBA interprets its constitution to mean that ousting Donald Sterling on June 3 would also automatically oust Shelly Sterling as co-owner, with the Clippers then falling under the control of commissioner Adam Silver. Donald Sterling’s proposed maneuver risks the prospect of Shelly Sterling undertaking a slow-moving effort to sell the team. A sale process that takes months or years would clearly aggravate the NBA, which wants to erase the Sterling family name from the league as quickly as possible. A protracted sale of the Clippers by Shelly Sterling might also constitute a potential rationale for players to boycott NBA games.

Even of greater risk to the NBA, what is to stop Shelly Sterling from deciding to keep the Clippers? She could plausibly reason, on various grounds, that now is not the right time to sell the team. Also, her instruction from her husband to sell the team would not be legally binding; it would be a mere suggestion the moment she takes over the team.

Read much more at the link.

Ta-Nehisi Coates

I’ll end with a long article that I haven’t gotten to yet, but I’m hearing it’s a must read: The Case for Reparations, by Ta-Nehisi Coates at The Atlantic. Here’s the tagline:

“Two hundred fifty years of slavery. Ninety years of Jim Crow. Sixty years of separate but equal. Thirty-five years of racist housing policy. Until we reckon with our compounding moral debts, America will never be whole.”

Some reactions:

The Guardian: The ‘Case for Reparations’ is solid, and it’s long past time to make them.

Slate: An Ingenious and Powerful Case for Reparations.

The Wire: You Should Read “The Case for Reparations.”

NPR: How To Tell Who Hasn’t Read The New ‘Atlantic’ Cover Story.

WaPo: Culture change and Ta-Nehisi Coates’s ‘The Case For Reparations’.

What else is happening? As always, please post your links in the comment thread.

Did you like this post? Please share it with your friends:

Recent Comments