Monday Afternoon Reads

Posted: July 6, 2015 Filed under: morning reads | Tags: Euro Eurozone, Germany, Greek Debt Crisis 27 CommentsGood Afternoon!

Sorry that this post has been taking so long. My computer is having a complete meltdown. I’m on my old one right now and it’s reallllllyyyyyy slowwwwww.

I want to spend a little time with the meltdown in Greece which is a complex situation. The most interesting source that I’ve found to date is an interview with French Economist Thomas Piketty with Germany’s Zeit Magazine. Last night, I read a good translation of the piece here. It’s been removed–temporarily hopefully–from the medium site so you’ll have to struggle through the bad German-English translation at Zeit’s site. The most interesting part of the interview is that Piketty explains the history of nations having to repay their debt after losing wars or under other circumstances. He explains that the European fixation with austerity and punishing Greece denies how German debt was handled post WW2 and the reality that forgiving German national debt helped Germany become what it is today. So, why are the Germans not extending the same courtesy to Greece?

Piketty: When I hear the Germans now say that they maintain a very moral dealing with debt and firmly believe that debts must be repaid, then I think: That’s a big joke! Germany is the country that has never paid his debts. It can be obtained in other countries no lessons.

TIME: Do you want to try the story in order to portray States who do not repay their debts as a winner?

Piketty: Just such a state is Germany. But slowly: The story teaches us two options for a highly indebted country to settle its arrears. One has fooled the British Empire in the 19th century after the Napoleonic Wars expensive: It’s slow method, which today also recommends Greece. The UK division at that time the debt through rigorous financial management from – although it worked, but took extremely long. Over 100 years the British relatives two to three percent of its economic output on the debt, spending more than they for schools and education.That must not be and should not be today. For the second method is much faster.Germany has it tried in the 20th century. Essentially, it consists of three components: inflation, a special tax on private assets and liabilities sections.

TIME: And now you want to tell us that our economic miracle was based on debt cuts that we deny the Greeks today?

Piketty: Exactly. The German government was in debt after the war ended in 1945 with more than 200 percent of its gross national product. Ten years later it had little choice but the national debt was less than 20 percent of the national product. France succeeded in that time a similar feat. This tremendously rapid debt reduction but we would never have reached with the budgetary resources that we recommend Greece today. Instead, our two countries turned to the second method, the three mentioned components, including debt restructuring. Think. To the London Debt Conference in 1953, canceled on the 60 percent of Germany’s foreign debt and also the domestic debt of the young Federal Republic were restructured

TIME: This was from the realization that the high repayment demands on Germany after the First World War on the grounds of the Second World Warincluded. They wanted this time forgive the Germans for their sins!

Piketty: Nonsense! This had nothing to do with moral insights, but was a rational economic decision. It was recognized at the time correctly: According to major crises which have a high debt burden result, there comes a time when you have to turn to the future. We can not expect to pay for decades for their parents’ mistakes of new generations. Now the Greeks have undoubtedly made great mistakes. By 2009, the government in Athens have forged their budgets. Why not the younger generation of Greeks now bears more responsibility for the mistakes of their parents as the young generation of Germans in the 1950s and 1960s. We must now look forward. Europe was founded on forgetting the debt and investing in the future. And it is not on the idea of eternal penance. We need to remember.

The Guardian similarly argues that what was good for Germany in 1953 is good for Greece today.

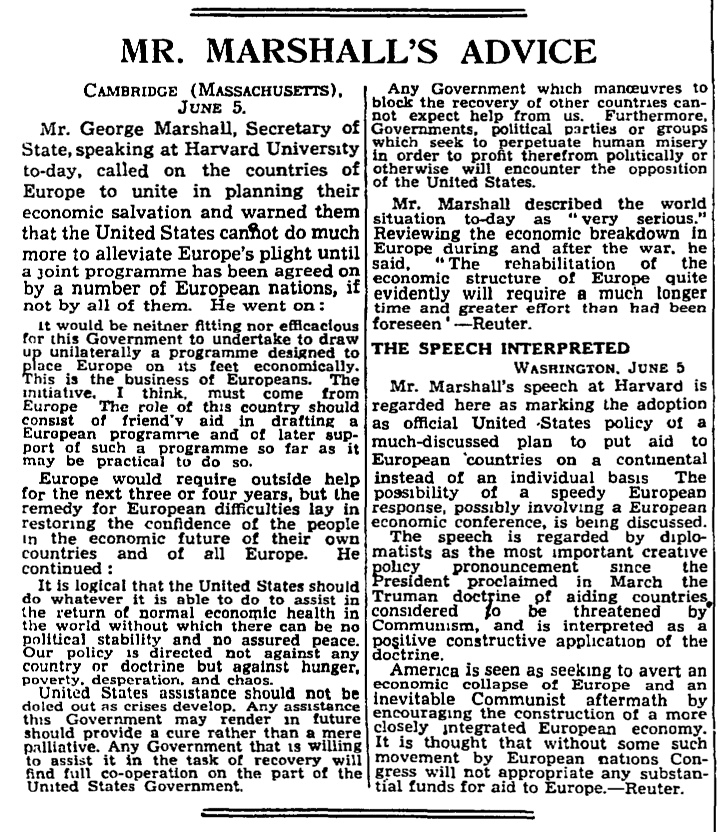

The arguments being used by the Greek government to secure debt relief can be traced back to a little-reported speech made to the students of Harvard University on 5 June 1947.

It was there that George Marshall, the then US secretary of state, floated the idea of a European programme of economic reconstruction. The Americans saw thatEurope was on the brink of economic collapse. Industrial capacity had been wiped out. Trade had ceased. People were going hungry and, in Marshall’s view, at risk of turning to communism.

Despite being the turning point for Europe’s economies after the second world war, Marshall’s speech was not considered as especially important at the time. The State Department did not bother to tell anybody in Europe about what he was about to say and the British embassy in Washington did not think it worth the cost to send a cable with an advance copy of the speech to London.

But the speech was covered by the BBC’s Washington correspondent and, by luck, his report was heard by the then UK foreign secretary, Ernest Bevin, in a wireless set he kept by his bedside. Bevin seized on the opportunity provided by the Americans, who said the Europeans had to organise their own plan for disbursing the money. “It was like a life line to sinking men,” he said later. “It seemed to bring hope where there was none.”

Lessons had been learned from the mistakes made after the first world war. Then, the victorious Allied powers had imposed a punitive peace on Germany, demanding heavy reparations that bred resentment.

Marshall tried a different approach. Over four years, the US pumped $13bn into Europe (the equivalent of more than $150bn today) in the hope that it would rebuild economic capacity, enable countries to trade with each other, and rebuff the threat from Stalin’s Soviet Union. It was not an entirely selfless act. The US at the time accounted for 50% of the world’s output, and needed to find markets for its exports. The lack of demand in countries such as France, Italy and Germany in 1947 meant this was not possible.

Britain was the single biggest beneficiary of Marshall aid, receiving more than a quarter of the total. Germany took $1.4bn (11% of the total), four times as much as Greece received.

Paul Krugman had some analysis and advice.

Paul Krugman had some analysis and advice.

The truth is that Europe’s self-styled technocrats are like medieval doctors who insisted on bleeding their patients — and when their treatment made the patients sicker, demanded even more bleeding. A “yes” vote in Greece would have condemned the country to years more of suffering under policies that haven’t worked and in fact, given the arithmetic, can’t work: austerity probably shrinks the economy faster than it reduces debt, so that all the suffering serves no purpose. The landslide victory of the “no” side offers at least a chance for an escape from this trap.<

But how can such an escape be managed? Is there any way for Greece to remain in the euro? And is this desirable in any case?The most immediate question involves Greek banks. In advance of the referendum, the European Central Bank cut off their access to additional funds, helping to precipitate panic and force the government to impose a bank holiday and capital controls. The central bank now faces an awkward choice: if it resumes normal financing it will as much as admit that the previous freeze was political, but if it doesn’t it will effectively force Greece into introducing a new currency.

Specifically, if the money doesn’t start flowing from Frankfurt (the headquarters of the central bank), Greece will have no choice but to start paying wages and pensions with i.o.u.s, which will de facto be a parallel currency — and which might soon turn into the new drachma.

Suppose, on the other hand, that the central bank does resume normal lending, and the banking crisis eases. That still leaves the question of how to restore economic growth.

In the failed negotiations that led up to Sunday’s referendum, the central sticking point was Greece’s demand for permanent debt relief, to remove the cloud hanging over its economy. The troika — the institutions representing creditor interests — refused, even though we now know that one member of the troika, the International Monetary Fund, had concluded independently that Greece’s debt cannot be paid. But will they reconsider now that the attempt to drive the governing leftist coalition from office has failed?

The European Central Bank (ECB)--which is akin to our FED for those countries in the EuroZone–has stated it will continue Emergency Liquidity Assistance to Greek Banks. However, they are imposing higher “haircuts”.

And the ECB has maintained the cap on emergency liquidity assistance (ELA) at €89bn, but crucially it has “adjusted” the haircuts it applies to the assets which Greek banks hand over in return for funds.

In simple terms, that probably means the ECB is treating Greek government bonds as riskier, and valuing them as such when it calculates how much liquidity it can provide.

It’s another tightening of the screw on Greece – meaning some banks may find it even tougher to qualify for emergency liquidity assistance.

This is from Robert Reich as posted to his Facebook page.

Five things you need to know about the Greek debt crisis as of now:

1. The Greek people voted correctly yesterday in rejecting more tax increases and spending cuts. They’ve already been punished too much by their creditors — mostly big banks, as represented by the IMF, European Central Bank, and European Commission.

2. Austerity was the wrong medicine to begin with. It put Greece into a death spiral of economic woe that worsened its debt crisis.

3. Now it’s up to the rest of Europe to respond. It’s in its interest to offer Greece easier bailout terms, and then help Greece get to work on what Greece has already agreed to do — reform its tax system so that wealthy Greeks can’t escape taxation, and reform its budget process to avoid political payoffs.

4. But if Europe doesn’t respond, the best of the worst cases to follow would be for Greece to withdraw from the euro. That will happen automatically if Greek banks issue IOUs instead of euros (cash is already being rationed), and those IOUs become, in effect, a different currency.

5. There could be “contagion” to Spain, Portugal, Ireland, and Italy if creditors fear future defaults and the incapacity of the eurozone to govern itself economically. That would hurt the United States, especially Wall Street, whose exposure to European banks is still considerable.

Greek’s Finance Minister Yanis Varoufakis has resigned.

Varoufakis was sidelined a week or so ago, not because of the “disrespectful” style of his jackets, but because of the directness of his argument. As the Greek prime minister Alexis Tsipras said, he speaks the language of economists better than they do.

He has always insisted that the responsibility for the Greek recovery did not lie with Greece alone, that there had to be realism in the conditions demanded by Greece’s creditors, as the sheer human cost was too much to bear. He showed how financial issues had become politicised, how the old paradigms were broken. Worse, he spoke to Eurocrats as equals.

He spoke to the rest of us as human beings, describing what Europe had laid on the shoulders of Greece as “fiscal waterboarding”. He railed at the birthplace of democracy being turned into what he called “a debt colony”.

As his heroic people last night rose up against “debt-bondage” he gave a press conference in a grey T-shirt and today announced his resignation, explaining that some Eurogroup participants don’t want him in the discussion. He says he does not care for the privilege of office but for collective support for Tsipras.

He is a man who walks like he talks, and that talk is open. This is so unlike the secretive deals usually made in airless rooms in Brussels. Here is a politician acting on his beliefs. He will be remembered not for his style, but for his substance. He faced down the automatons by insisting the Greek people should no longer be punished. And his people were with him. He refused the Eurocrats’ parameters and secrecy. He spoke with decency, and not in code. He is not afraid of the word “collective”. Nor is Syriza. Tsipras has said “negotiation does not belong to one person, it never did”. It is possible that Varoufakis was pushed rather than jumped, to smooth a deal, but whatever the case, he will not disappear, even as he revs off into the sunset. He knows, above all, that real style is substance. He saved his best look for last when he said, “I shall wear the creditors’ loathing with pride”.

I’m going to close this post with a quote from Lenin who wrote about the role of banks at the highest stage of capitalism which is supposed to lead to collapse from his viewpoint. I just always find it an interesting read whenever I see how concentrated the banking sector has become. I’m not a Marxist but I always love a bit of insight when it’s so, well insightful.

As banking develops and becomes concentrated in a small number of establishments, the banks grow from modest middlemen into powerful monopolies having at their command almost the whole of the money capital of all the capitalists and small businessmen and also the larger part of the means of production and sources of raw materials in any one country and in a number of countries. This transformation of numerous modest middlemen into a handful of monopolists is one of the fundamental processes in the growth of capitalism into capitalist imperialism; for this reason we must first of all examine the concentration of banking.

…These simple figures show perhaps better than lengthy disquisitions how the concentration of capital and the growth of bank turnover are radically changing the significance of the banks. Scattered capitalists are transformed into a single collective capitalist. When carrying the current accounts of a few capitalists, a bank, as it were, transacts a purely technical and exclusively auxiliary operation. When, however, this operation grows to enormous dimensions we find that a handful of monopolists subordinate to their will all the operations, both commercial and industrial, of the whole of capitalist society; for they are enabled-by means of their banking connections, their current accounts and other financial operations—first, to ascertain exactly the financial position of the various capitalists, then to control them, to influence them by restricting or enlarging, facilitating or hindering credits, and finally to entirely determine their fate, determine their income, deprive them of capital, or permit them to increase their capital rapidly and to enormous dimensions, etc.

Greece never met the convergence criteria for legitimate membership in the EuroZone. That’s an interesting story in itself. Now, the question is will they stay or will they go and how will all of this impact the EURO monetary union?

Independence Day Reads

Posted: July 4, 2011 Filed under: Bailout Blues, Domestic Policy, Economy, Foreign Affairs, Global Financial Crisis, Greece, investment banking, morning reads | Tags: Bill Clinton, Budget Deficit, debt limit, Fukushima, Greek Debt Crisis, John McCain, nuclear crisis, shadow banking industry, SIVs, taxes 16 Comments Happy Independence Day!

Happy Independence Day!

We have a republic and a lot of people have sacrificed a lot over the last several centuries to keep it. Too bad most of our politicians aren’t in that number. They can’t see past their next elections.

It seems that two senators– McCain and Corynyn–say they’re open to tax increases as a way to solve the budget stand off. Guess there are a few of them left that would prefer not to tank our economy. Let’s hope this starts some real negotiations instead of the usual Republican hostage taking and Democratic cave-in that’s been politics as usual the last dozen years or so.

One of the senators, John Cornyn of Texas, said he would consider eliminating some tax breaks and corporate subsidies in the context of changes in the tax code, provided there was not an overall increase in taxes.

“I think it’s clear that the Republicans are opposed to any tax hikes, particularly during a fragile economic recovery,” Mr. Cornyn said on “Fox News Sunday.” “Now, do we believe tax reform is necessary? I would say absolutely.”

But he insisted that any changes in taxes be “revenue neutral,” meaning that the government would not take in any more money from individuals or businesses than it does now.

The other senator, John McCain of Arizona, said he would be willing to consider some “revenue raisers” as part of a broad deal, but he refused to name specific measures.

Mr. Cornyn, a member of the Senate leadership, also said that Republicans would be open to a short-term deal on the debt ceiling to provide more time for a comprehensive agreement.

Let’s also hope that more reasonable and less ideological heads prevail on the right and that the left stands up for what’s right for a change. Former President Clinton had a words of policy advice over the weekend. His advice to President Obama is “not to blink”.

Former President Bill Clinton Saturday night urged President Obama not to “blink” at Republican demands to exclude revenue increases from any agreement to extend the government’s debt ceiling.

If Republicans maintain their opposition to revenue increases, Clinton said, Obama should pursue a short-term deal to extend the debt ceiling based on spending cuts both sides have already accepted in the negotiations between the administration and Congressional leaders from both parties.

“I hope they will make a mini-deal,” Clinton said in an interview conducted with him at the Aspen Ideas Festival here.

The White House and Congressional negotiators from both parties are attempting to assemble a deficit reduction package that could win support in Congress for legislation to extend the nation’s debt ceiling, which the Treasury says the government will reach on August 2. The talks have foundered amid demands from Congressional Republicans to exclude any revenue increases from that prospective deficit reduction package.

Asked what the administration could do if GOP leaders hold to that posture, Clinton replied: “First the White House could blink. I hope that won’t happen. I don’t think they should blink.”

If Republicans will not accept revenues in a package to lift the debt ceiling by August 2, Clinton said, Obama should pursue a short-term agreement based on the spending reductions both sides have already accepted.

“There are some spending cuts they agree on …and he can take those and [get] an extension of the debt ceiling for six or eight months,” Clinton said.

Clinton also called on a package of reforms to US tax policy that includes a corporate tax cut if special interest tax loops are closed. This is something Obama has also supported.

“It made sense when I did it. It doesn’t make sense anymore – we’ve got an uncompetitive rate. We tax at 35 percent of income, although we only take about 23 percent. So, we SHOULD cut the rate to 25 percent, or whatever’s competitive, and eliminate a lot of the deductions so that we still get a FAIR amount, and there’s not so much variance in what the corporations pay. But how can they do that by Aug. 2?”

Clinton also said Grover Norquist, who as president of Americans for Tax Reform is the GOP’s unofficial enforcer of no-new-taxes pledges, has a “chilling” hold on the nation’s lawmaking.

The former president said it has seemed like Republicans need any revenue concessions need to be “approved in advance by Grover Norquist.”

“You’re laughing,” he told the crowd of 800. “But he was quoted in the paper the other day saying he gave Republican senators PERMISSION … on getting rid of the ethanol subsidies. I thought, ‘My GOD, what has this country come to when one person has to give you permission to do what’s best for the country.’ It was chilling.

There’s an extremely interesting piece at The Atlantic Wire on “What Really Happened at Fukushima”. It includes interviews with workers that have been inside the crippled nuclear plant.

Throughout the months of lies and misinformation, one story has stuck: “The earthquake knocked out the plant’s electric power, halting cooling to its reactors,” as the government spokesman Yukio Edano said at a March 15 press conference in Tokyo. The story, which has been repeated again and again, boils down to this: “after the earthquake, the tsunami – a unique, unforeseeable [the Japanese word is soteigai] event – then washed out the plant’s back-up generators, shutting down all cooling and starting the chain of events that would cause the world’s first triple meltdown to occur.”

But what if recirculation pipes and cooling pipes, burst, snapped, leaked, and broke completely after the earthquake — long before the tidal wave reached the facilities, long before the electricity went out? This would surprise few people familiar with the 40-year-old Unit 1, the grandfather of the nuclear reactors still operating in Japan.

The authors have spoken to several workers at the plant who recite the same story: Serious damage to piping and at least one of the reactors before the tsunami hit. All have requested anonymity because they are still working at the plant or are connected with TEPCO. One worker, a 27-year-old maintenance engineer who was at the Fukushima complex on March 11, recalls hissing and leaking pipes. “I personally saw pipes that came apart and I assume that there were many more that had been broken throughout the plant. There’s no doubt that the earthquake did a lot of damage inside the plant,” he said. “There were definitely leaking pipes, but we don’t know which pipes – that has to be investigated. I also saw that part of the wall of the turbine building for Unit 1 had come away. That crack might have affected the reactor.”

The reactor walls of the reactor are quite fragile, he notes. “If the walls are too rigid, they can crack under the slightest pressure from inside so they have to be breakable because if the pressure is kept inside and there is a buildup of pressure, it can damage the equipment inside the walls so it needs to be allowed to escape. It’s designed to give during a crisis, if not it could be worse – that might be shocking to others, but to us it’s common sense.”

Here’s some frightening news on the disaster in Japan. Radioactive Cesium has been found in Tokyo’s water supply.

Radioactive cesium-137 was found in Tokyo’s tap water for the first time since April as Japan grapples with the worst nuclear disaster in 25 years.

Cesium-137 concentration registered at 0.14 becquerels per kilogram in the city’s Shinjuku ward on July 2, compared with 0.21 becquerels on April 22, according to the Tokyo Metropolitan Institute of Public Health. No cesium-134 or iodine-131 was detected, the agency said on its website.

The Nuclear Safety Commission of Japan sets a safety limit of 200 becquerels per kilogram for cesium-134 and cesium-137. The limit for iodine-131 consumption is 300 becquerels per kilogram.

Japan is battling radiation leaks into the air, soil and water after an earthquake and tsunami on March 11 knocked out cooling systems at Tokyo Electric Power Co.’s Fukushima Dai- Ichi nuclear station, resulting in the meltdown of three of the six reactors at the plant.

The UK Guardian lists an interesting set of Greek public assets for sale. Many have no buyers. Bobby Jindal is putting up a lot of Louisiana assets for sale too. I wonder if this is going to be the new way to raise money. The Kochs already rent a big chunk of Yellowstone. Let’s hope we don’t have to put our national treasures on the chopping block.

Up for sale are 39 airports, 850 ports, railways, motorways, sewage works, a couple of energy companies, banks, defence groups, thousands of acres of land for development, casinos and Greece’s national lottery. George Christodoulakis, Greece’s special secretary for asset restructuring and privatisations, said the sell-off would raise €50bn (£44bn) to help pay back the country’s €110bn bailout debt.

The private equity bosses gathered in the hotel’s ballroom for the parade of Greece’s national treasures showed little interest in buying anything.

Nikos Stathopoulous, managing partner of BC Partners, which has invested more than €3.5bn in Greece, said investors are put off by bureaucracy, strong unions, corruption and a lack of transparency. “Even in the good times Greece is not a country that attracts investment. Foreign investors don’t want to invest in a country where there is no flexibility in hiring and firing people,” he said. “You don’t want to invest in a country in which you wake up and a new law has been passed which totally undermines and destroys the value of the investment you’ve just made.”

Stathopoulous said investors were finding it very hard to assess the risk of investing into Greece, which means assets “will be priced at lower than they are worth, lower than the Greek government, and even the European Union, expects”.

Here’s a compelling argument for getting the shadow banking sector into a more regulated, transparent, and standardized order. It’s written by Henry Tabe who is a Founding Partner of Sequoia Investment Management Company Ltd. It particularly addresses the use of the Structured Investment Vehicle (SIV). Complex, nonstandard, and unregulated markets make pricing assets difficult and introduce unnecessary risk and volatility.

Risk management requires identification, measurement, aggregation, and effective management of risks. It should help businesses allocate sufficient capital for survival and growth. The SIV’s extinction highlights risk management failures by the vehicles, their sponsors, rating agencies, policymakers, and regulators.

Financial regulators permitted bank, insurance company, pension, and hedge-fund sponsors to establish SIV “mini-banks” without ensuring that they maintain sufficient capital or back-stop liquidity in the event of a run. Policymakers also seemed unaware of the knock-on effects of the SIV’s demise on the securitisation and global credit markets. The Financial Security Authority’s call for regulators to incorporate sectoral analytical capabilities in their micro-prudential policies should help close the knowledge gap and ensure that timely solutions can be implemented to avert collapses that engender significantly more stress on the financial system (FSA 2009).

Lessons learned include the tightening of regulation governing the sponsorship of off-balance-sheet structures and the sizing of their capital and liquidity needs. These require that regulators adopt a more proactive, dampening role in the wild swings from exuberance to despair that are so characteristic of the financial markets. Discussions around contingent capital and similar products suggest regulators have embraced that dampening role and moved away from the prevailing pre-crisis philosophy of minimal regulation.

Lessons learned also include closer supervision of shadow banks, more skin-in-the-game for their sponsors, in-house retention of risk-analytics capabilities by investors, and less reliance on credit-rating agencies. The agencies themselves are more tightly supervised in order to reduce ratings shopping by issuers and inherent conflicts of interest in the business model (CESR 2009). Tighter regulation will also help to ensure that the agencies improve the monitoring of analyst performance, qualifications, and experience (Dodd-Frank 2010).

These measures should help restore confidence in rating agencies and the global financial system, an outcome more urgently required given on-going turmoil in the sovereign debt market.

So, there’s some wonky goodness to keep you entertained if you’re inside today. Be sure to let us know what you’re reading and blogging! Hope your Fourth of July is a happy one!

Friday Reads

Posted: June 17, 2011 Filed under: morning reads | Tags: ACORN, Budget talks, DIAPERS David Vitter, Fort Calhoun Nuclear Plant, Greek Debt Crisis, hypocrisy, Joe Biden, Lehman meltdown, Oiled Pelicans living in Georgia 16 Comments Good Morning!

Good Morning!

Political witch hunts are interesting things. Ask me. One of my senators used his senate cell phone to call up and hire prostitutes from the infamous Washington Madam. He’s still in the U.S. Senate after he made his wife beg the press to stop hounding the family and spent a summer fleeing any and all press. The calls from Republican leadership for his resignation never came, yet Senator David Vitter broke the law and was caught with his “diapers down”. Where’s the media outrage over this pervert?

So, here’s another story about a Breitbart Witch Hunt. A report by the “GAO Finds Little to Support Congress’ Abolition of ACORN: Grass-roots consumer organization was driven into bankruptcy by conservative critics”. This was the predecessor to the current attacks on Planned Parenthood. Unsubstantiated lies bandied about by partisan news outlets appear to be able to successfully take out liberal organizations and people.

A report issued today by the Government Accountability Office(GAO) finds little to support the charges that led to the demise of the Association of Community Organizations for Reform Now (ACORN), a grassroots consumer advocacy organization driven out of existence by Congressional critics.

The GAO found that monitoring of awards to ACORN by government agencies generally consisted of reviewing progress reports and making site visits. Of 22 investigations of alleged election and voter registration fraud, most were closed without prosecution, the report found.

One of eight investigations of alleged voter registration fraud resulted in guilty pleas and seven were closed without action due to lack of evidence.

When will Democratic leadership and the press stand up to these witch hunts?

Robert Scheer has an excellent piece in The Nation called “The Seven Republican Dwarfs”. He points out at how the Republican candidates in the Presidential run are willfully ignorant of economic reality. He doesn’t spare Obama either.

Obama, who has been inconsistent and weak in reining in the Wall Street greed that got us into this deep economic morass, is now under no pressure from the opposition to improve his performance. The Republican knee-jerk reaction—government bad, big business great, and don’t dare say that the Wall Street scoundrels who created this crisis need a timeout—gets Obama off the hook from legitimate criticism he needs to hear. As the Wall Street Journal headlined the non-debate: “Candidates Run Against Regulation.”

It’s as if the sound government regulation of the financial industry implemented in response to the Great Depression—not its polar opposite, the radical deregulation fueled by Republican free market zealots—was the source of our banking meltdown.

It’s only a matter of time before we experience similar problems. It may come this summer if the game of playing chicken with US sovereign debt continues. We shouldn’t be Greece but we are being set up to suffer their current fate by the inability of political leaders to do the right thing instead of the politically expedient thing. The financial community is calling the current Greece situation the EU’s “Lehman moment”. We may have a second Lehmann moment coming up shortly. If bond vigilantes don’t see progress in US debt ceiling talks shortly, we may be facing increased borrowing costs. Right now, the flee from Greece is helping us. This disaster probably will not hurt the US unless the contagion goes from Greece to Ireland to Portugal and on to Spain. However, many tea party Republicans seem hell bent on recreating the post-Lehman meltdown.

The euro lost more than 2 percent against the dollar in the past two days and the cost of protecting corporate bonds soared to the highest level since January, with credit-default swaps anticipating about a 78 percent chance that Greece won’t pay its debts. Equities declined around the world, while a measure of fear in fixed-income markets jumped the most since November.

Market moves suggest heightened concern that authorities won’t be able to keep Greece’s debt troubles from spreading after Moody’s Investors Service said it may downgrade BNP Paribas SA and two other big French banks because of their investments in the southern European nation. The collapse of Lehman Brothers Holdings Inc. in September 2008 caused credit markets worldwide to freeze as investors fled all but the safest government debt.

“The probability of a eurozone Lehman moment is increasing,” said Neil Mackinnon, an economist at VTB Capital in London and a former U.K. Treasury official. “The markets have moved from simply pricing in a high probability of a Greek debt default to looking at a scenario of it becoming disorderly and of contagion spreading to other economies like Portugal, like Ireland, and maybe Spain, Italy and Belgium.”

VP Biden held talks with his bi-partisan gang of six on Thursday. He characterized the talks as progressing but also mentioned their are significant differences between the two parties.

Vice President Joe Biden said Thursday that he and congressional negotiators have done a “first serious scrub” of the entire federal budget but differences remain over big-ticket items that philosophically divide the two parties in their quest for an agreement that would raise the nation’s debt ceiling while putting in place long-term reductions to the nation’s $14.3 trillion debt.

Those big-ticket items include whether to increase tax revenues – which many Democrats want – and making changes to expensive entitlements like Medicare – which many Republicans support.

“Everybody wants an agreement,” Biden told reporters after a meeting in the Capitol with the bipartisan group of lawmakers and other top Obama administration officials. “That is sufficiently realistic to get to $4 trillion over a decade or so – in terms of reductions.”

He said the group would meet four days next week, as opposed to three days this week, and that each meeting would be longer than the two hours or so each meeting has been to date. He also said their staffs would work “around the clock” to support the talks.

There’s some good news for the Arabian Oryx. This is a fascinating herd animal that has been pulled back from the brink of  distinction.

distinction.

Believed by many to be the inspiration behind the legends of the unicorn, the Arabian oryx, Oryx leucoryx, is a species of antelope believed to be hunted to extinction in the wild in the 1970s.

However, with the help of the captive breeding program of the International Union for Conservation of Nature (IUCN), the species has been reintroduced into the wild, and a population has now grown back to 1,000 individuals.

The creature, known locally as Al Maha, jumped three categories on the IUCN Red List of Threatened Species from “Extinct in the Wild” to “Vulnerable,” an unprecedented accomplishment.

“To have brought the Arabian Oryx back from the brink of extinction is a major feat and a true conservation success story, one which we hope will be repeated many times over for other threatened species,” says Razan Khalifa Al Mubarak, Director General of the Environment Agency-Abu Dhabi, in a press release.

“It is a classic example of how data from the IUCN Red List can feed into on-the-ground conservation action to deliver tangible and successful results.”

Other good news for animals comes from Georgia where Pelicans that were coated with Oil from the Gulf Oil Gusher have found a new home. The brown Pelicans have no only survived, they have laid some eggs!

Brown pelicans that survived being covered in oil during the April 2010 spill in Louisiana are laying eggs and having babies on Georgia’s coast, according to wildlife officials, Savannah Morning News reports. Hundreds of the birds were scrubbed clean following the disaster and moved to Georgia and other states. Wildlife officials were not sure if they would live, much less have babies. But they did, and they are, and wildlife officials are thrilled.

Tim Keyes, a coast bird biologist with the Georgia Department of Natural Resources has reported what could be the first known successful nesting of brown pelicans at Little Egg Island Bar, a state-protected wildlife area about 60 miles south of Savannah, according to the newspaper’s website savannahnow.com.

Keyes told the newspaper Wednesday he has counted 17 brown pelican chicks since May spread among eight nests tended by a parent that survived the oil spill. The birds were identified as having been removed from the spill and released in Georgia by bands placed around their legs.

Nebraska has a nuclear plant that sits north of Omaha on the flooding Missouri River. A breech has already occurred in a downstream levee and is flooding Hamburg, Iowa. How safe is the plant? Well,historically, not very and it’s now on a yellow alert. Here’s some information from the Bulletin of Atomic Scientists.

The Nuclear Regulatory Commission (NRC) issued a “yellow finding PDF” (indicating a safety significance somewhere between moderate and high) for the plant last October, after determining that the Omaha Public Power District (OPPD) “did not adequately prescribe steps to mitigate external flood conditions in the auxiliary building and intake structure” in the event of a worst-case Missouri River flood. The auxiliary building — which surrounds the reactor building like a horseshoe flung around a stake — is where the plant’s spent-fuel pool and emergency generators are located.

OPPD has since taken corrective measures, including sealing potential floodwater-penetration points, installing emergency flood panels, and revising sandbagging procedures. It’s extremely unlikely that this year’s flood, no matter how historic, will turn into a worst-case scenario: That would happen only if an upstream dam were to instantaneously disintegrate. Nevertheless, in March of this year the NRC identified Fort Calhoun as one of three nuclear plants requiring the agency’s highest level of oversight. In the meantime, the water continues to rise.

Yup, my youngest daughter is spending the summer with my oldest daughter not very far from the plant. Believe me, I’m not happy about all of the information provided in that report. You should definitely read the link because it seems the press aren’t reporting anything about the problem plant.

So, that’s what’s been on my computer screen this morning! What’s on your reading and blogging list today?

{kind=link}

Recent Comments