Monday Afternoon Reads

Posted: July 6, 2015 Filed under: morning reads | Tags: Euro Eurozone, Germany, Greek Debt Crisis 27 CommentsGood Afternoon!

Sorry that this post has been taking so long. My computer is having a complete meltdown. I’m on my old one right now and it’s reallllllyyyyyy slowwwwww.

I want to spend a little time with the meltdown in Greece which is a complex situation. The most interesting source that I’ve found to date is an interview with French Economist Thomas Piketty with Germany’s Zeit Magazine. Last night, I read a good translation of the piece here. It’s been removed–temporarily hopefully–from the medium site so you’ll have to struggle through the bad German-English translation at Zeit’s site. The most interesting part of the interview is that Piketty explains the history of nations having to repay their debt after losing wars or under other circumstances. He explains that the European fixation with austerity and punishing Greece denies how German debt was handled post WW2 and the reality that forgiving German national debt helped Germany become what it is today. So, why are the Germans not extending the same courtesy to Greece?

Piketty: When I hear the Germans now say that they maintain a very moral dealing with debt and firmly believe that debts must be repaid, then I think: That’s a big joke! Germany is the country that has never paid his debts. It can be obtained in other countries no lessons.

TIME: Do you want to try the story in order to portray States who do not repay their debts as a winner?

Piketty: Just such a state is Germany. But slowly: The story teaches us two options for a highly indebted country to settle its arrears. One has fooled the British Empire in the 19th century after the Napoleonic Wars expensive: It’s slow method, which today also recommends Greece. The UK division at that time the debt through rigorous financial management from – although it worked, but took extremely long. Over 100 years the British relatives two to three percent of its economic output on the debt, spending more than they for schools and education.That must not be and should not be today. For the second method is much faster.Germany has it tried in the 20th century. Essentially, it consists of three components: inflation, a special tax on private assets and liabilities sections.

TIME: And now you want to tell us that our economic miracle was based on debt cuts that we deny the Greeks today?

Piketty: Exactly. The German government was in debt after the war ended in 1945 with more than 200 percent of its gross national product. Ten years later it had little choice but the national debt was less than 20 percent of the national product. France succeeded in that time a similar feat. This tremendously rapid debt reduction but we would never have reached with the budgetary resources that we recommend Greece today. Instead, our two countries turned to the second method, the three mentioned components, including debt restructuring. Think. To the London Debt Conference in 1953, canceled on the 60 percent of Germany’s foreign debt and also the domestic debt of the young Federal Republic were restructured

TIME: This was from the realization that the high repayment demands on Germany after the First World War on the grounds of the Second World Warincluded. They wanted this time forgive the Germans for their sins!

Piketty: Nonsense! This had nothing to do with moral insights, but was a rational economic decision. It was recognized at the time correctly: According to major crises which have a high debt burden result, there comes a time when you have to turn to the future. We can not expect to pay for decades for their parents’ mistakes of new generations. Now the Greeks have undoubtedly made great mistakes. By 2009, the government in Athens have forged their budgets. Why not the younger generation of Greeks now bears more responsibility for the mistakes of their parents as the young generation of Germans in the 1950s and 1960s. We must now look forward. Europe was founded on forgetting the debt and investing in the future. And it is not on the idea of eternal penance. We need to remember.

The Guardian similarly argues that what was good for Germany in 1953 is good for Greece today.

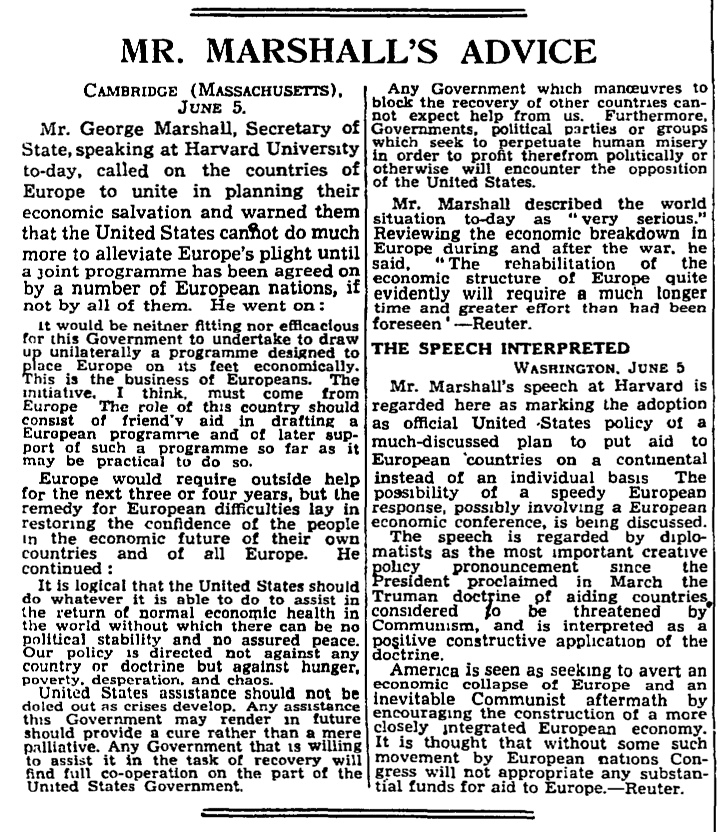

The arguments being used by the Greek government to secure debt relief can be traced back to a little-reported speech made to the students of Harvard University on 5 June 1947.

It was there that George Marshall, the then US secretary of state, floated the idea of a European programme of economic reconstruction. The Americans saw thatEurope was on the brink of economic collapse. Industrial capacity had been wiped out. Trade had ceased. People were going hungry and, in Marshall’s view, at risk of turning to communism.

Despite being the turning point for Europe’s economies after the second world war, Marshall’s speech was not considered as especially important at the time. The State Department did not bother to tell anybody in Europe about what he was about to say and the British embassy in Washington did not think it worth the cost to send a cable with an advance copy of the speech to London.

But the speech was covered by the BBC’s Washington correspondent and, by luck, his report was heard by the then UK foreign secretary, Ernest Bevin, in a wireless set he kept by his bedside. Bevin seized on the opportunity provided by the Americans, who said the Europeans had to organise their own plan for disbursing the money. “It was like a life line to sinking men,” he said later. “It seemed to bring hope where there was none.”

Lessons had been learned from the mistakes made after the first world war. Then, the victorious Allied powers had imposed a punitive peace on Germany, demanding heavy reparations that bred resentment.

Marshall tried a different approach. Over four years, the US pumped $13bn into Europe (the equivalent of more than $150bn today) in the hope that it would rebuild economic capacity, enable countries to trade with each other, and rebuff the threat from Stalin’s Soviet Union. It was not an entirely selfless act. The US at the time accounted for 50% of the world’s output, and needed to find markets for its exports. The lack of demand in countries such as France, Italy and Germany in 1947 meant this was not possible.

Britain was the single biggest beneficiary of Marshall aid, receiving more than a quarter of the total. Germany took $1.4bn (11% of the total), four times as much as Greece received.

Paul Krugman had some analysis and advice.

Paul Krugman had some analysis and advice.

The truth is that Europe’s self-styled technocrats are like medieval doctors who insisted on bleeding their patients — and when their treatment made the patients sicker, demanded even more bleeding. A “yes” vote in Greece would have condemned the country to years more of suffering under policies that haven’t worked and in fact, given the arithmetic, can’t work: austerity probably shrinks the economy faster than it reduces debt, so that all the suffering serves no purpose. The landslide victory of the “no” side offers at least a chance for an escape from this trap.<

But how can such an escape be managed? Is there any way for Greece to remain in the euro? And is this desirable in any case?The most immediate question involves Greek banks. In advance of the referendum, the European Central Bank cut off their access to additional funds, helping to precipitate panic and force the government to impose a bank holiday and capital controls. The central bank now faces an awkward choice: if it resumes normal financing it will as much as admit that the previous freeze was political, but if it doesn’t it will effectively force Greece into introducing a new currency.

Specifically, if the money doesn’t start flowing from Frankfurt (the headquarters of the central bank), Greece will have no choice but to start paying wages and pensions with i.o.u.s, which will de facto be a parallel currency — and which might soon turn into the new drachma.

Suppose, on the other hand, that the central bank does resume normal lending, and the banking crisis eases. That still leaves the question of how to restore economic growth.

In the failed negotiations that led up to Sunday’s referendum, the central sticking point was Greece’s demand for permanent debt relief, to remove the cloud hanging over its economy. The troika — the institutions representing creditor interests — refused, even though we now know that one member of the troika, the International Monetary Fund, had concluded independently that Greece’s debt cannot be paid. But will they reconsider now that the attempt to drive the governing leftist coalition from office has failed?

The European Central Bank (ECB)--which is akin to our FED for those countries in the EuroZone–has stated it will continue Emergency Liquidity Assistance to Greek Banks. However, they are imposing higher “haircuts”.

And the ECB has maintained the cap on emergency liquidity assistance (ELA) at €89bn, but crucially it has “adjusted” the haircuts it applies to the assets which Greek banks hand over in return for funds.

In simple terms, that probably means the ECB is treating Greek government bonds as riskier, and valuing them as such when it calculates how much liquidity it can provide.

It’s another tightening of the screw on Greece – meaning some banks may find it even tougher to qualify for emergency liquidity assistance.

This is from Robert Reich as posted to his Facebook page.

Five things you need to know about the Greek debt crisis as of now:

1. The Greek people voted correctly yesterday in rejecting more tax increases and spending cuts. They’ve already been punished too much by their creditors — mostly big banks, as represented by the IMF, European Central Bank, and European Commission.

2. Austerity was the wrong medicine to begin with. It put Greece into a death spiral of economic woe that worsened its debt crisis.

3. Now it’s up to the rest of Europe to respond. It’s in its interest to offer Greece easier bailout terms, and then help Greece get to work on what Greece has already agreed to do — reform its tax system so that wealthy Greeks can’t escape taxation, and reform its budget process to avoid political payoffs.

4. But if Europe doesn’t respond, the best of the worst cases to follow would be for Greece to withdraw from the euro. That will happen automatically if Greek banks issue IOUs instead of euros (cash is already being rationed), and those IOUs become, in effect, a different currency.

5. There could be “contagion” to Spain, Portugal, Ireland, and Italy if creditors fear future defaults and the incapacity of the eurozone to govern itself economically. That would hurt the United States, especially Wall Street, whose exposure to European banks is still considerable.

Greek’s Finance Minister Yanis Varoufakis has resigned.

Varoufakis was sidelined a week or so ago, not because of the “disrespectful” style of his jackets, but because of the directness of his argument. As the Greek prime minister Alexis Tsipras said, he speaks the language of economists better than they do.

He has always insisted that the responsibility for the Greek recovery did not lie with Greece alone, that there had to be realism in the conditions demanded by Greece’s creditors, as the sheer human cost was too much to bear. He showed how financial issues had become politicised, how the old paradigms were broken. Worse, he spoke to Eurocrats as equals.

He spoke to the rest of us as human beings, describing what Europe had laid on the shoulders of Greece as “fiscal waterboarding”. He railed at the birthplace of democracy being turned into what he called “a debt colony”.

As his heroic people last night rose up against “debt-bondage” he gave a press conference in a grey T-shirt and today announced his resignation, explaining that some Eurogroup participants don’t want him in the discussion. He says he does not care for the privilege of office but for collective support for Tsipras.

He is a man who walks like he talks, and that talk is open. This is so unlike the secretive deals usually made in airless rooms in Brussels. Here is a politician acting on his beliefs. He will be remembered not for his style, but for his substance. He faced down the automatons by insisting the Greek people should no longer be punished. And his people were with him. He refused the Eurocrats’ parameters and secrecy. He spoke with decency, and not in code. He is not afraid of the word “collective”. Nor is Syriza. Tsipras has said “negotiation does not belong to one person, it never did”. It is possible that Varoufakis was pushed rather than jumped, to smooth a deal, but whatever the case, he will not disappear, even as he revs off into the sunset. He knows, above all, that real style is substance. He saved his best look for last when he said, “I shall wear the creditors’ loathing with pride”.

I’m going to close this post with a quote from Lenin who wrote about the role of banks at the highest stage of capitalism which is supposed to lead to collapse from his viewpoint. I just always find it an interesting read whenever I see how concentrated the banking sector has become. I’m not a Marxist but I always love a bit of insight when it’s so, well insightful.

As banking develops and becomes concentrated in a small number of establishments, the banks grow from modest middlemen into powerful monopolies having at their command almost the whole of the money capital of all the capitalists and small businessmen and also the larger part of the means of production and sources of raw materials in any one country and in a number of countries. This transformation of numerous modest middlemen into a handful of monopolists is one of the fundamental processes in the growth of capitalism into capitalist imperialism; for this reason we must first of all examine the concentration of banking.

…These simple figures show perhaps better than lengthy disquisitions how the concentration of capital and the growth of bank turnover are radically changing the significance of the banks. Scattered capitalists are transformed into a single collective capitalist. When carrying the current accounts of a few capitalists, a bank, as it were, transacts a purely technical and exclusively auxiliary operation. When, however, this operation grows to enormous dimensions we find that a handful of monopolists subordinate to their will all the operations, both commercial and industrial, of the whole of capitalist society; for they are enabled-by means of their banking connections, their current accounts and other financial operations—first, to ascertain exactly the financial position of the various capitalists, then to control them, to influence them by restricting or enlarging, facilitating or hindering credits, and finally to entirely determine their fate, determine their income, deprive them of capital, or permit them to increase their capital rapidly and to enormous dimensions, etc.

Greece never met the convergence criteria for legitimate membership in the EuroZone. That’s an interesting story in itself. Now, the question is will they stay or will they go and how will all of this impact the EURO monetary union?

{kind=link}

Recent Comments