Finally Friday Reads: Backpfeifengesicht

Posted: March 7, 2025 Filed under: Economy, Equity Markets, FARTUS, kakistocracy, MAGA Assholes, MAGA Political Carnage, Polycrisis, Psychopaths in charge | Tags: a face worthy of being slapped, Backpfeifengesicht, CryptoCurrency Ponzi Scheme from Trump and Musk, Declaration of Independence, FARTUS, martial-law, People are not Illegal, Space X explosion, The Insurrection Act, White Male Christian Supremacists 8 Comments

“EEK!” John Buss, @repeat1968, @johnbuss.bsky.social

Good Day, Sky Dancers!

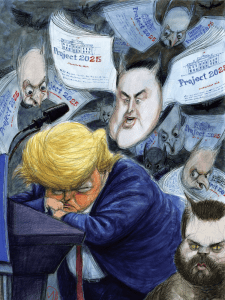

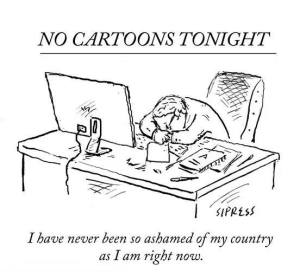

Backpfeifengesicht is the German word for “a face worthy of being slapped.” That might be the most usable word in the dark timeline, which is the second term of #FARTUS (Felon, Adjudicated Rapist, Traitor of the United States). JJ found this sweet article at The Guardian and shared it with BB and me this morning. It’s an Op-Ed written by Marina Hyde about JD Vance, but it could apply to any subhuman of the modern MAGA movement. “There are 1,000 grotesque memes of JD Vance – and they’re all more likable than the real thing. Angry, rude and addicted to web troll-ery, the vice-president has the Make America Awful Again portfolio. Seems a perfect fit.” Ayup.

You may well be aware that Backpfeifengesicht is the German word for a face that is worthy of being slapped. Even so, how has this not been internationalised? Or at the very least Americanised, where its dictionary definition would presumably be adorned by a picture of the face of US vice-president JD Vance – already faultlessly playing the role of worst American at your hotel. You can immediately picture him at breakfast, can’t you? Every single other guest on the terrace with their shoulders up round their ears, just thinking: “Where is he now? How unbearable is he being NOW?” Next, imagine breakfast lasting four years.

I say the Backpfeifengesicht definition would be accompanied by JD Vance’s face … but then again, what is the face of JD Vance? The internet is awash with people suffering an acute case of not being able to remember it any more, having seen so many hideous comic distortions of Vance that those meme versions are not simply the only results on the first page of your own mental Google search, but stretch deep beyond the second and into the third. Somewhere on page four, where you might as well publish the nuclear codes or pictures of Taylor Swift giving cocaine to babies, is an unmodified snap of what JD Vance actually looks like. Or at least what he looks like with eyeliner.

Before you get there – and you don’t, really – your synaptic filing systems throw up every variety of Photoshopped Vancefake: swollen manboy, face wearing a Minion suit, a bearded egg … I’m hoping that sooner or later, an American news outlet will accidentally use a modified photo, because even the picture editor has forgotten what the vice-president looks like, and then we can have one of those massively self-regarding legacy media-blow-ups, where the entire staff has to resign after a remorseless investigation by the executive editor reveals Vance isn’t actually a big purple grape. “This is a stain on our newspaper’s history. A big purple stain.”

Vance is more meme than man, now, and it is, of course, something of a consolation that he is so extremely online that he can’t help but have noticed this. The VP is like a one-man government troll-feeding programme – please don’t cut him, Elon! – which is probably why people have become so heroically committed to taking the piss. The probability of the vice-president seeing you insulting him is basically one.

Just as previous holders of his office like Teddy Roosevelt and Richard Nixon once did, Vance spent a notable amount of this week both denying he suggested Britain and France were random countries that hadn’t fought a war in 40 years, and replying to random X posters called things like “Jeff Computers” to counter the suggestion that he wasn’t loved and feted on his recent skiing holiday.

While JJ found that amusing read today. BB brought home the rancid bacon. This is an op-ed by Brett Wagner in The San Francisco Chronicle today. “Is Trump preparing to invoke the Insurrection Act? Signs are pointing that way. A joint Department of Defense and Homeland Security report will soon recommend whether or not to invoke the Insurrection Act over illegal migration.”

While JJ found that amusing read today. BB brought home the rancid bacon. This is an op-ed by Brett Wagner in The San Francisco Chronicle today. “Is Trump preparing to invoke the Insurrection Act? Signs are pointing that way. A joint Department of Defense and Homeland Security report will soon recommend whether or not to invoke the Insurrection Act over illegal migration.”

The clock is ticking down on a crucial but little-noticed part of President Donald Trump’s first round of executive orders — the one tasking the secretaries of the Department of Defense and Department of Homeland Security to submit a joint report, within 90 days, recommending “whether to invoke the Insurrection Act.”

Many of us are now holding our collective breath, knowing that the report and what it contains could put us on the slippery slope toward unchecked presidential power under a man with an affinity for ironfisted dictators.

Adding to the suspense was the recent “Friday Night Massacre” at the Pentagon — the firing of the nation’s top uniformed officer and removing other perceived guardrails (i.e., the top uniformed lawyers at the Army, Navy and Air Force) standing between the president and his long-stated intention to declare martial law upon returning to power.

Coincidence?

As we wait to find out, this would be a good time to take a closer look.

Say, for example, that Trump were to invoke the Insurrection Act and declare martial law. He wouldn’t even be required, by the letter of the law, to allege an “insurrection.” All that would be required is to assert that “unlawful obstruction” has made it “impracticable to enforce the laws of the United States” (as President Dwight D. Eisenhower did when he ordered the Arkansas National Guard to enforce the desegregation of Little Rock, Ark., schools).

This is where all the false claims and outright lies Trump and his political allies have been pushing will come into play: Trump falsely alleging, for example, that an entire city in Colorado has been taken over by Venezuelan street gangs, that a city in Ohio has been overrun by Haitian refugees who are eating all the cats and dogs, and other vague assertions that “millions and millions” of “illegals” are pouring into our country every week (or “day” depending on who’s telling the lie at the moment).

Each of these false claims and outright lies could be distilled, to declare martial law, into catchy phrases (beginning with the legalese word “Whereas”) to establish the legal premise for invoking the Insurrection Act, and to lay the predicate to begin going door-to-door, wherever they please, under the pretense of searching for undocumented immigrants who don’t exist.

I bring you the reality on the ground from Joy Reid on Threads. “This is inhumane, hideous and repugnant. If this is what MAGA America is, count me out. I’m ashamed that this is what our government is doing. Shame on them. Shame.” What it is is a 21-year-old girl with cancer who relies completely on her immigrant mother, who is in no way a criminal or bothering anyone. When protesters came to protest, they were arrested. How many laws and constitutional rights can this miserable administration break before they completely break all of us? This story comes from El Monte, California. You can read the hatred of the MAGA monsters in the threads below on YouTube. I’ve gotten to the point where I don’t want to leave the house and take a chance at seeing a FARTUS supporter in my neighborhood. I’m fine with all the immigrants, though. Everything they do makes my neighborhood a better place.

“I can’t even wake up properly… she helps me, she bathes me, she changes me, she makes my food.”Deportation didn’t protect anyone it only stole a mother from the child who needs her most-Blake Coronadowww.threads.net/@blakecorona…

— Audrey (@parickards.bsky.social) 2025-03-06T23:59:31.294Z

The US Military and US Vets are under attack from this Administration. This cannot be denied. This is from the AP this morning. FARTUS has always had a thing against military service and those who fight for values that he seems to hate very much. “War heroes and military firsts are among 26,000 images flagged for removal in Pentagon’s DEI purge.” So much of this just comes as an attack against the diversity of our nation being represented in all of its institutions. But is that really it? Why the disappearance of all people of color, women, and the LGBTQ community? Are white cis men really that sensitive?

The US Military and US Vets are under attack from this Administration. This cannot be denied. This is from the AP this morning. FARTUS has always had a thing against military service and those who fight for values that he seems to hate very much. “War heroes and military firsts are among 26,000 images flagged for removal in Pentagon’s DEI purge.” So much of this just comes as an attack against the diversity of our nation being represented in all of its institutions. But is that really it? Why the disappearance of all people of color, women, and the LGBTQ community? Are white cis men really that sensitive?

References to a World War II Medal of Honor recipient, the Enola Gay aircraft that dropped an atomic bomb on Japan and the first women to pass Marine infantry training are among the tens of thousands of photos and online posts marked for deletion as the Defense Department works to purge diversity, equity and inclusion content, according to a database obtained by The Associated Press.

The database, which was confirmed by U.S. officials and published by AP, includes more than 26,000 images that have been flagged for removal across every military branch. But the eventual total could be much higher.

One official, who spoke on condition of anonymity to provide details that have not been made public, said the purge could delete as many as 100,000 images or posts in total, when considering social media pages and other websites that are also being culled for DEI content. The official said it’s not clear if the database has been finalized.

Defense Secretary Pete Hegseth had given the military until Wednesday to remove content that highlights diversity efforts in its ranks following President Donald Trump’s executive order ending those programs across the federal government.

The vast majority of the Pentagon purge targets women and minorities, including notable milestones made in the military. And it also removes a large number of posts that mention various commemorative months — such as those for Black and Hispanic people and women.

Are they just trying to up their odds that one will be less likely to disrupt the plan when martial law is declared? Everything they’ve been doing shows their delight in being the worst kind of bullies. Just yesterday, they announced they will deport Ukrainians who fled to the US for safety. We are no longer a safe harbor. Not even close. Heather Cox Richardson discusses this in detail this morning in her Substack Letters from an American.

Are they just trying to up their odds that one will be less likely to disrupt the plan when martial law is declared? Everything they’ve been doing shows their delight in being the worst kind of bullies. Just yesterday, they announced they will deport Ukrainians who fled to the US for safety. We are no longer a safe harbor. Not even close. Heather Cox Richardson discusses this in detail this morning in her Substack Letters from an American.

This morning, Ted Hesson and Kristina Cooke of Reuters reported that the Trump administration is preparing to deport the 240,000 Ukrainians who fled Russia’s attacks on Ukraine and have temporary legal status in the United States. Foreign affairs journalist Olga Nesterova reminded Americans that “these people had to be completely financially independent, pay tax, pay all fees (around $2K) and have an affidavit from an American person to even come here.”

“This has nothing to do with strategic necessity or geopolitics,” Russia specialist Tom Nichols posted. “This is just cruelty to show [Russian president Vladimir] Putin he has a new American ally.”

The Trump administration’s turn away from traditional European alliances and toward Russia will have profound effects on U.S. standing in the world. Edward Wong and Mark Mazzetti reported in the New York Times today that senior officials in the State Department are making plans to close a dozen consulates, mostly in Western Europe, including consulates in Florence, Italy; Strasbourg, France; Hamburg, Germany; and Ponta Delgada, Portugal, as well as a consulate in Brazil and another in Turkey.

In late February, Nahal Toosi reported in Politico that President Donald Trump wants to “radically shrink” the State Department and to change its mission from diplomacy and soft power initiatives that advance democracy and human rights to focusing on transactional agreements with other governments and promoting foreign investment in the U.S.

Elon Musk and the “Department of Government Efficiency” have taken on the process of cutting the State Department budget by as much as 20%, and cutting at least some of the department’s 80,000 employees. As part of that project, DOGE’s Edward Coristine, known publicly as “Big Balls,” is embedded at the State Department.

As the U.S. retreats from its engagement with the world, China has been working to forge greater ties. China now has more global diplomatic posts than the U.S. and plays a stronger role in international organizations. Already in 2025, about 700 employees, including 450 career diplomats, have resigned from the State Department, a number that normally would reflect a year’s resignations.

Shutting embassies will hamper not just the process of fostering goodwill, but also U.S. intelligence, as embassies house officers who monitor terrorism, infectious disease, trade, commerce, militaries, and government, including those from the intelligence community. U.S. intelligence has always been formidable, but the administration appears to be weakening it.

Trump, bitcoin, political cartoon

We’re being turned into part of the Trump Grift Mafia. Nothing will be left standing of any of the good we have done in the world. This is neocolonialism and neomercantilism. We’ve retreated to some of the worst historical ideologies ever. The most symbolic thing happened yesterday. The latest Space X project blew up in the sky and shut down many flights yesterday. “Breakup of SpaceX’s Starship Rocket Disrupts Florida Airports. The video showed the upper stage of the most powerful rocket ever built spinning out of control in space, a repeat of an unsuccessful test flight in January that led to debris falling over the Caribbean.” This is what we’re spending money for? Elonia is pushing his company to the brink of getting to Mars and looking down at the rest of us. The report is from The New York Times‘s Kenneth Chang.

Starship — the huge spacecraft that Elon Musk says will one day take people to Mars — failed during its latest test flight on Thursday when its upper stage exploded in space, raining debris and disrupting air traffic at airports from Florida to Pennsylvania.

It was the second consecutive test flight of the most powerful rocket ever built where the upper-stage spacecraft malfunctioned. It started spinning out of control after several engines went out and then lost contact with mission control.

Photographs and videos posted on the social media site X by users saying they were along the Florida coast showed the spacecraft breaking up. The falling debris disrupted flights at airports in Miami, Orlando, Palm Beach and Fort Lauderdale, and as far away as Philadelphia International Airport.

The Starship rocket system is the largest ever built. At 403 feet tall, it is nearly 100 feet taller than the Statue of Liberty atop its pedestal.

It has the most engines ever in a rocket booster: The Super Heavy booster is powered by 33 of SpaceX’s Raptor engines. As those engines lift Starship off the launchpad, they will generate 16 million pounds of thrust at full throttle.

The upper part, also called Starship or Ship for short, looks like a shiny rocket from science fiction movies of the 1950s, is made of stainless steel with large fins. This is the upper stage that will head toward orbit, and ultimately could carry people to the moon or even Mars.

The rocket lifted off a little after 6:30 p.m. Eastern time on Thursday from the SpaceX site known as Starbase at the southern tip of Texas near the city of Brownsville.

Starship’s mammoth booster again successfully returned to the launchpad, just as it had during the previous test flight. In the last half minute before the upper-stage engines were to shut off, several of them malfunctioned. Video from the rocket showed a tumbling view of Earth and space until it cut off.

Ashley Parker and Michael Scherer wrote this analysis for The Atlantic. “Trump’s Own Declaration of Independence. The president, who has flirted with regal rhetoric, wants a historic copy of America’s founding document placed in the Oval Office.”

Long live the king!

Down with the king!

President Donald Trump sees the appeal of both.

Trump jokingly declared himself a sovereign last month, while his advisers distributed AI-generated photos of him wearing a crown and an ermine robe to celebrate his order to end congestion pricing in New York City. “He who saves his Country does not violate any Law,” he’d decreed a few days earlier, using a phrase sometimes attributed to Napoleon Bonaparte, the emperor of the French.

I had no idea one of my greats who signed the Declaration had made of the copies of it. But the weird thing here is that Trump seriously wants the document to hang in the Oval Office. My question is, why take it from the people who can see it in the archives?

I had no idea one of my greats who signed the Declaration had made of the copies of it. But the weird thing here is that Trump seriously wants the document to hang in the Oval Office. My question is, why take it from the people who can see it in the archives?

Since returning to power, Trump has moved quickly to redesign his working space. He has announced plans to pave over the Rose Garden to make it more like the patio at his private Mar-a-Lago club, as well as easier to host events with women wearing heels. He has also revived planning for a new ballroom on the White House grounds. “It keeps my real-estate juices flowing,” Trump explained in a recent interview with The Spectator.

Golden trophies now line the Oval Office’s mantlepiece. Military flags adorned with campaign streamers have returned. And portraits of presidents past now climb the walls—George Washington, Thomas Jefferson, John Adams, Martin Van Buren, Theodore Roosevelt, Franklin D. Roosevelt, and Ronald Reagan, among others. Gilded mirrors hang upon the recessed doors. A framed copy of his Georgia mug shot appears in the outside hallway. And the bright-red valet button, encased in a wooden box, is back on the desk.

In addition to the National Archives’ original Declaration, the government has in its possession other versions of the document. The collection includes drafts by Jefferson and copies of contemporaneous reprintings, known as broadsides, that were distributed among the colonies.

Alarmed by the deterioration of the original Declaration in the 1820s, Secretary of State John Quincy Adams commissioned William J. Stone to create an engraving of it with the signatures appended. That version forms the basis of the document since reproduced in school history books—the one with which most Americans are familiar. Adams tasked Stone with engraving 200 copies—but in what passes for a mini 19th-century scandal, Stone made an extra facsimile to keep for himself, the documents dealer and expert Seth Kaller told us.

Many of those Stone copies of the document have now been lost; roughly 50 are known to survive, Kaller said. The White House already has in its archives at least one of the Stone printings. Kaller told us that one of his clients who had recently purchased a Stone facsimile was visiting the White House when President Barack Obama asked him whether he could help procure a Stone printing for the White House.

“The client called me, and I said, ‘I can’t—because, one, there aren’t any others on the market right now, and two, the White House already has one,’” Kaller told us. In 2014, Kaller visited the White House to view the Stone Declaration, which the curator displayed for him in one of the West Wing’s rooms. (The White House curator’s office did not respond to multiple requests for comment, including on whether the Stone copy still resides under its purview.)

It is unclear where Trump first got the idea to add a Declaration to the Oval Office’s decor. Since returning, Trump has shown interest in the planning for celebrations next year of the 250th anniversary of the document’s signing. Days after taking office, he issued an executive order to create “Task Force 250,” a White House commission that will work with another congressionally formed commission to plan the festivities.

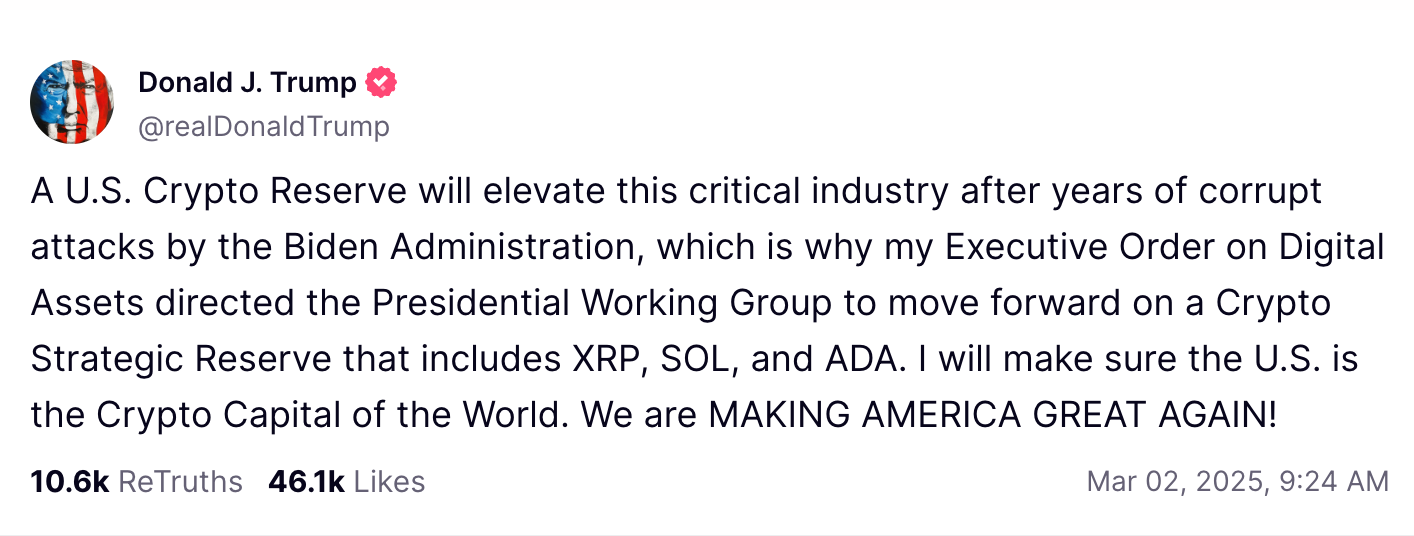

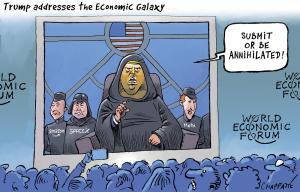

I hope he’s not trying to go with one of those grandiose military parades again. And if he does, will he eliminate everyone but the white guys? It can’t be anything other than another way for him to get attention, that’s for sure. Again, this all continues to be an appalling cosplay of how FARTUS wants to view himself in relation to his imagined ideas of American History. I can’t even with the economy today. Just know he’s changed his mind on tariffs again for Canada and Mexico, and employment figures are worsening. He’s turned a strong economy into a weak one in a matter of weeks. He’s also shaken the Equity markets to their core. What’s on is this: “Trump’s “Crypto Reserve” is a world historical grift. Corruption doesn’t get much more blatant than this.” My Finance Daughter and I both find crypto to be a huge Ponzi scheme. I lecture against it. She doesn’t consider it a product that brokers should be involved in. In short, we stay as far away as possible. But, you know, grifters gotta grift. This is from Public Notice.

Authoritarian regimes by definition have no accountability to voters or the public. That means autocrats and their cronies can gorge themselves at the public trough and blatantly steal from taxpayers with few if any consequences.

It’s not really a surprise, then, that as part of his authoritarian power grab, Trump has embraced brazen and open self-dealing. The most ludicrous example of this is the scheme he announced last Sunday for a national crypto reserve.

As with many of Trump’s big orange dreams, it’s not exactly clear what the crypto reserve will entail or how it will work. But the brilliance of the half-baked idea is that Trump and his cronies can make bank just by talking about it. The president can use his bully pulpit to manipulate markets. And who’s going to stop him?

Trump, fresh off avoiding 88 felony charges, obviously feels confident that the answer is “no one.”

Government on the blockchain

Crypto refers to digital currencies which are generated and stored in a digital ledger, or blockchain. In theory, cryptocurrencies do not rely on a central government authority. Proponents say they are useful for quick or anonymous transactions. Critics point out that cryptocurrency seems designed for hiding illegal transactions and/or creating what are essentially Ponzi investment schemes.

Because of the downsides, President Biden created moderate guidelines to try to regulate some of the worst excesses of the industry, which made him an enemy of hardcore crypto boosters. But Trump in his first term expressed even deeper skepticism about cryptocurrencies, saying they are based on “thin air.”

During the 2024 election, though, crypto investors spent tens of millions on Republican campaigns. Trump, who never saw a quid pro quo he didn’t love, changed his tune, embracing crypto-friendly policies. After his victory, he followed through by appointing venture capitalist and Elon Musk crony David Sacks as a White House crypto czar.

Another reason Trump flip-flopped on crypto is that his family figured out how to cash in. Following the election, Trump squandered some of the goodwill he had built up with the crypto industry when he and his wife Melania launched memecoins — essentially valueless crypto confidence games — that both surged in value, making the Trumps billions (but undermining the credibility of crypto in the process). That came after his two adult sons, Eric and Don Jr, launched their own crypto company during the campaign called World Liberty Financial. Boosting crypto as president, then, allows Trump and his family to profit directly from his public office.

Trump announced his thank you to the industry last Sunday, when he declared that he would create a “Crypto Strategic Reserve” in order to make the US “the Crypto Capital of the World.” He of course claimed the move is part of “MAKING AMERICA GREAT AGAIN.”

But the actual point of the crypto reserve, much less the details, are sketchy at best. Proponents argue crypto is a store of value, like gold, and could help damp inflation. But the major cryptocurrencies tend to rise and fall in value based on broader macroeconomic sentiment. And since crypto is volatile and, unlike gold, has no intrinsic value, it’s hard to credit its usefulness as a currency stabilizer.

If you have any questions about any of this, I’d be glad to try to answer them. Seeing such craziness in our economic policy has been hard on me. I’m just waiting for the major attack on the Federal Reserve Bank. They’re the only ones that bring credibility to the dollar these days, and I’m afraid he’ll have a go at them. The mess at the Treasury is already impacting the banking business. Don’t even get me started on the Budget Crisis, either. I’m tired of the repeats of that one by disingenuous Republicans.

I hope all of you can close your doors and stay sane inside the one place you can control, home. I have a few more tests next week, so I will be out at clinics again, being poked and prodded. This weekend, I will just relax and try to avoid the ever-changing Trump Surreality Show.

What’s on your reading and blogging list today?

Mostly Monday Reads: VIllainy! Winning!

Posted: March 3, 2025 Filed under: #FARTUS, American Fascists, Equity Markets, kakistocracy, MAGA Assholes, MAGA Political Carnage, Political and Editorial Cartoons, Polycrisis, Psychopaths in charge | Tags: @johnbuss.bsky.social John Buss, CryptoCurrency Ponzi Scheme from Trump and Musk, Elderly and Vets, FARTUS, Starving Children, Trump Tariffs 13 Comments

“Honorable Douche Member.” John Buss, @repeat1968, @johnbuss.bsky.social

Good Day, Sky Dancers!

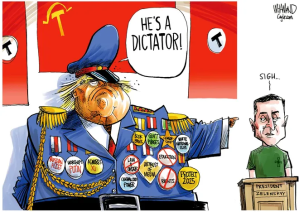

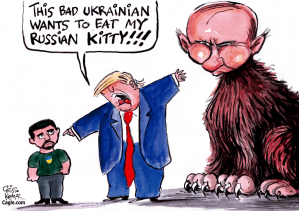

Once again, the transformation of American democracy into a theocratic fascist state–which once was unimaginable–is shaking global confidence. The closing argument came Friday when #FARTUS and JDank tried to shake down Ukraine’s President like a classic Mafia Don. The US is no longer the leader of the free world. We are becoming the lap dog of evil men.

It was further announced that the dollar will no longer be the world’s currency as the Bad Men of faithless investments are rolling back protections and trying to install the Ponzi scheme of the century–cryptocurrency–as something it can never be. This dodgy investment does not meet any of the criteria that define money. It cannot be used as a universal means of exchange. It has no role as a store of value. Indeed, it is quite a risky gamble. It does not represent a measure of exchange. Help us, Federal Reserve Board of Governors! You may be the only chance because the Treasury’s Rules and Regulations, which were based on stopping another Great Depression, are being dismantled even as we speak.

William Kristol, Andre Egger, and Sam Stein had this headline at The Bulwark that rang true to me this morning. “What a Weekend for Putin! It’s been a long time since the Russian dictator had it this good.” All enemies of the USA and democracy had a good week. All those with greed as a defining characteristic are likely celebrating. I’m certainly glad I moved my 403(B) money to the Eurozone. They were slow coming off COVID-19, but they’re getting stronger while we are getting economically, militarily, and democratically weaker by the drop of every grain of sand.

It was a hell of a weekend for bad men getting what they paid for out of Donald Trump. And while we’ll focus on Vladimir Putin here, we don’t want to fully ignore venture capitalist David Sacks, Donald Trump’s “crypto czar,” who seemingly stands to make bank following Trump’s weekend announcement of a “strategic cryptocurrency reserve.” Hey, we’re glad someone’s having fun. Happy Monday.

Helluva Weekend doesn’t even cover the outrage heard around the country. However, it appears it’s getting a little late in the game to shut down this offensive move on the American Experiment. Just seeing the polling and the angry constituents all over the country over the Zelinsky Shake Down should’ve lit a fire under the proud party of Chicken Hawks. It didn’t. We have more evidence of chickens than hawks. This is also part of The Bulwark’s Monday Money Quarter-backing.

Helluva Weekend doesn’t even cover the outrage heard around the country. However, it appears it’s getting a little late in the game to shut down this offensive move on the American Experiment. Just seeing the polling and the angry constituents all over the country over the Zelinsky Shake Down should’ve lit a fire under the proud party of Chicken Hawks. It didn’t. We have more evidence of chickens than hawks. This is also part of The Bulwark’s Monday Money Quarter-backing.

SEE ROGER RUN: How to cope with all the grisly news? One increasingly common strategy: Blowing off some steam by yelling at your Republican lawmaker.

On Saturday, Kansas Sen. Roger Marshall became the latest victim of this hot new trend at an overstuffed town hall in the small town of Oakley (pop. ~2000). Attendees booed his arrival and rolled their eyes at his answers throughout the prickly hour-long event, while Marshall castigated them as “rude.” He suggested they’d fallen victim to “misinformation” about DOGE and ultimately cut the event short.

A possible opportunity for introspection for the senator? Apparently not. In a statement, Marshall’s office suggested the fix was in, the town hall “sabotaged” by “Democrat operatives.” “Real Kansans,” the statement continued, “overwhelmingly support President Trump’s DOGE initiative.”

It was true that some attendees had schlepped to the event from the Kansas City area to give Marshall a piece of their mind. But some of their concerns were plainly shared by locals. The last crowd comment came, according to local media, from local resident Chuck Nunn, who politely and sorrowfully mourned DOGE’s reckless slashing of veteran jobs. Identifying himself as “a dying breed, a conservative Democrat,” Nunn said he supported the mission of identifying waste in government—but that “the way that we are going about it is so wrong, because there are unintended consequences.”

“What the government is doing right now, as far as cutting out those jobs, a huge percentage of those people—and I know you care about the veterans—are veterans,” Nunn went on. “And that’s a damn shame. A damn shame.”

Acting like this sentiment is nothing but scurrilous left-wing astroturf may be comforting to Republicans. But it’s also remarkably short-sighted. There’s a reason “do right by our veterans” has long been a more or less universal tenet of our politics. Scoffing off that extremely normie critique of the DOGEbros is something Republicans do at their peril.

If you think that’s bad, check out the opinions of House Leader Mike Johnson. No Republican has been left out of this party. Heather Cox Richardson has another example of Mike Johnson’s inability to lead or take a stand for our country. He’s staked out the coward’s gavel. She wrote this yesterday in her Substack Letters From an American.

If you think that’s bad, check out the opinions of House Leader Mike Johnson. No Republican has been left out of this party. Heather Cox Richardson has another example of Mike Johnson’s inability to lead or take a stand for our country. He’s staked out the coward’s gavel. She wrote this yesterday in her Substack Letters From an American.

On Face the Nation this morning, Representative Mike Turner (R-OH), a strong supporter of the North Atlantic Treaty Organization (NATO) and Ukraine, contradicted that information. “Considering what I know, what Russia is currently doing against the United States, that would I’m certain not be an accurate statement of the current status of the United States operations,” he said. Well respected on both sides of the aisle, Turner was in line to be the chair of the House Intelligence Committee in this Congress until House speaker Mike Johnson (R-LA) removed him from that slot and from the intelligence committee altogether.

And yet, as Stephanie Kirchgaessner of The Guardian notes, the Trump administration has made clear that it no longer sees Russia as a cybersecurity threat. Last week, at a United Nations working group on cybersecurity, representatives from the European Union and the United Kingdom highlighted threats from Russia, while Liesyl Franz, the State Department’s deputy assistant secretary for international cybersecurity, did not mention Russia, saying the U.S. was concerned about threats from China and Iran.

Kirchgaessner also noted that under Trump, the Cybersecurity and Infrastructure Security Agency (CISA), which monitors cyberthreats against critical infrastructure, has set new priorities. Although Russian threats, especially those against U.S. election systems, were a top priority for the agency in the past, a source told Kirchgaessner that analysts were told not to follow or report on Russian threats.

“Russia and China are our biggest adversaries,” the source told Kirchgaessner. “With all the cuts being made to different agencies, a lot of cybersecurity personnel have been fired. Our systems are not going to be protected and our adversaries know this.” “People are saying Russia is winning,” the source said. “Putin is on the inside now.”

Another source noted that “There are dozens of discrete Russia state-sponsored hacker teams dedicated to either producing damage to US government, infrastructure and commercial interests or conducting information theft with a key goal of maintaining persistent access to computer systems.” “Russia is at least on par with China as the most significant cyber threat, the person added. Under those circumstances, the source said, ceasing to follow and report Russian threats is “truly shocking.”

Trump’s outburst in the Oval Office on Friday confirmed that Putin has been his partner in politics since at least 2016. “Putin went through a hell of a lot with me,” Trump said. “He went through a phony witch hunt where they used him and Russia… Russia, Russia, Russia—you ever hear of that deal?—that was a phony Hunter Biden, Joe Biden, scam. Hillary Clinton, shifty Adam Schiff, it was a Democrat scam. And he had to go through that. And he did go through it, and we didn’t end up in a war. And he went through it. He was accused of all that stuff. He had nothing to do with it. It came out of Hunter Biden’s bathroom.”

Putin went through a hell of a lot with Trump? It was an odd statement from a U.S. president, whose loyalty is supposed to be dedicated to the Constitution and the American people.

Jen Ruben writes this at The Contrarian. “It’s not Dickens—it’s the MAGA agenda. Taking food from children; healthcare from the informed.” The #FARTUS team has already destroyed our soft power with the end of USAID. Next up is Medicaid, Medicare, and Social Security. Get your gardens started now! Cruelty is the mission.

Jen Ruben writes this at The Contrarian. “It’s not Dickens—it’s the MAGA agenda. Taking food from children; healthcare from the informed.” The #FARTUS team has already destroyed our soft power with the end of USAID. Next up is Medicaid, Medicare, and Social Security. Get your gardens started now! Cruelty is the mission.

Given the scope of the MAGA assault on the foundations of our democracy, many Democrats, responsible media outlets, and concerned Americans have (understandably) been focused on its attempt to obliterate the rule of law, the separation of powers, and the First Amendment. But we should never lose track of the abject immorality that is part and parcel of an ideology based on vengeful victimhood, conspiracy-mongering, and repudiation of science.

From the outbreak of measles to stalling grants to the pursuit of cures for “diseases ranging from heart disease and cancer to Alzheimer’s and allergies” to renewing the starvation crisis in Sudan to devasting cuts at the Veterans Administration to dismissal of patriotic, highly-trained trans members of the armed services…we cannot miss this administration’s abject cruelty; its almost-boisterous disregard for human life and dignity.

House and Senate Republicans bear just as much responsibility as President in Name Only (PINO) Donald Trump and acting president Elon Musk for mutely going along with these actions. Moreover, we must view the House budget as yet another exercise in cruelty and reckless endangerment of human life.

“Trump and Musk have slashed roughly 2,400 VA jobs…A decision that won’t make things more efficient, like they claimed, but will actually lead to longer wait times, more backlog and more chaos for Veterans,” Senator Tammy Duckworth (D-Illinois.) recently said at a virtual town hall. “They’ve also launched a wider purge of federal workers—firing, in total, an estimated 6,000 Veterans, includingthe folks behind the Veterans Crisis Line.” She emphasized, “The only reason they are doing this is to try to find enough loose change behind the couch cushions so that they can give even bigger tax breaks to the rich guys they pal around with on the golf course.”

Breaking the sacred obligation to care for our veterans is only one aspect of the onslaught. Perhaps the most egregious is the plan to slash $880B from Medicaid. The argument that cuts of that magnitude can be achieved by “reform” or by cutting “waste, fraud, and abuse,” frankly, insults our intelligence.

The impact of such cuts is immense given the reach of Medicaid. The Kaiser Family Foundation notes, “Medicaid is the primary program providing comprehensive health and long-term care to one in five people living in the U.S. and accounts for nearly $1 out of every $5 spent on health care.” Medicaid covers not only the poorest Americans, but seniors’ long-term health care, drug addicts, and the disabled. More than 72 million Americans are enrolled in some aspect of the program.

Whatever funds they’ve raised by the deaths and disposal of humanity, they will turn over to Greedy Billionaires and Businesses. However, the focus right now is still on #FARTUS upending World Order. This is from Vox’s Nicole Narea. “How Trump upended the world order, over one weekend A hectic 48 hours in Europe-Ukraine-US-Russia relations, explained.

Whatever funds they’ve raised by the deaths and disposal of humanity, they will turn over to Greedy Billionaires and Businesses. However, the focus right now is still on #FARTUS upending World Order. This is from Vox’s Nicole Narea. “How Trump upended the world order, over one weekend A hectic 48 hours in Europe-Ukraine-US-Russia relations, explained.

A blowup at the White House on Friday proved a rude awakening for some of the US’s closest partners in Europe, and left them scrambling to contemplate a world in which they can no longer be sure that the US is a reliable ally in Russia’s war on Ukraine.

In the wake of President Donald Trump and his team accosting Ukrainian President Volodymyr Zelenskyy in a heated, televised exchange in the Oval Office, European leaders met to devise a plan for protecting Ukraine from Russian aggression absent any security guarantees from the US.

And though multiple leaders, from UK Prime Minister Keir Starmer to NATO leader Mark Rutte, insisted that they still view the US as an important partner, the meeting nevertheless seemed like it might mark the abrupt beginning of a new Western world order — one in which Europe stands alone.

The UK and France have led efforts in recent weeks to advance Ukraine’s cause and to convince Trump to keep Ukraine’s (and Europe’s) best interests in mind as he attempts to craft a ceasefire or peace deal in Russia’s years-long war on Ukraine.

Sunday, Starmer presided over a summit of more than a dozen mostly European leaders and announced that the attendees would form a “coalition of the willing” to defend Ukraine and strengthen Europe’s military capabilities.

“Not every nation will feel able to contribute but that can’t mean that we sit back,” Starmer said. “Instead, those willing will intensify planning now with real urgency.”

That coalition could lead to UK troops on the ground in Ukraine as part of a peacekeeping force, should a ceasefire or peace deal come about, Starmer said. France and the UK reportedly have a ceasefire framework that Zelenskyy said he’s been briefed on.

Starmer did emphasize, however, that many in the group, including the UK, believe lasting peace will not be possible without US support. And while Starmer said he had a productive conversation with Trump about Ukraine this weekend, it’s not clear that US support will materialize.

That’s in part because the Trump administration and its allies reiterated throughout the weekend that they believe their current approach to peace — that is, holding talks with Russia sans Ukraine and blaming Ukraine for the war — is the right one. Trump adviser Elon Musk suggested on X that the US contemplate leaving the NATO security alliance.

The Trump team also redoubled their attacks on Zelenskyy on Sunday, with some going so far as to suggest the Ukrainian president ought to be replaced.

So, I will get to some of the economic impact of Trump’s Tariff Mania. I hope you don’t need a new car, just for starters. This is from Bloomberg. “Car Prices Are Poised for $12,000. Surge on Trump’s New Tariffs.”

So, I will get to some of the economic impact of Trump’s Tariff Mania. I hope you don’t need a new car, just for starters. This is from Bloomberg. “Car Prices Are Poised for $12,000. Surge on Trump’s New Tariffs.”

Impending tariffs on Canada and Mexico risk driving up US car prices by as much as $12,000, further squeezing consumers and wreaking havoc across the intricate web of automotive supply lines spanning the continent.

The cost to build a crossover utility vehicle will rise by at least $4,000, while the increase would be three times that for an electric vehicle examined in a new study from Anderson Economic Group, an automotive consultant in East Lansing, Michigan. And those costs would likely be passed on to consumers, the study found.

“That kind of cost increase will lead directly — and I expect almost immediately — to a decline in sales of the models that have the biggest trade impacts,” Patrick Anderson, chief executive officer of Anderson Economic Group, said in an interview.

These are some more depressing headlines concerning our economy and prices.

From CNN: “Trump’s tariff chaos threatens an economy already flashing yellow lights.”

Layoffs are rising. Consumer spending — the backbone of the economy — unexpectedly dropped in January. Consumer confidence has plunged. A key GDP forecast suddenly turned negative. And extreme fear is back on Wall Street as stocks slide.

Despite the murky picture, President Donald Trump continues to inject chaos into the economy with almost-constant tariff threats.

Now he’s just hours away from lobbing tariffs on not just one or two but all three of America’s biggest trading partners.

Starting on Tuesday, Trump has vowed to impose a 25% tariff on imported goods from Mexico and Canada, and to double tariffs on those from China to 20%.

Those tariffs — if they get imposed — could increase costs for Americans at a time when inflation remains stubbornly high. That, in turn, could prevent the Federal Reserve from lowering borrowing costs, another source of pain in the cost-of-living problem confronting consumers.

Mexico and Canada have all vowed to retaliate by slapping their own tariffs on US goods, setting the stage for a potential trade war inside of North America. China has promised to respond to higher tariffs, too.

From the New York Times: “A Key Interest Rate Falls, but Not for the Reasons Trump Wanted. Investors’ increasingly gloomy sentiment about economic growth appears to be driving down the 10-year Treasury yield.” That’s our safe haven investment btw.

From the New York Times: “A Key Interest Rate Falls, but Not for the Reasons Trump Wanted. Investors’ increasingly gloomy sentiment about economic growth appears to be driving down the 10-year Treasury yield.” That’s our safe haven investment btw.

President Trump campaigned on a promise to bring down interest rates. And he has fulfilled that pledge in one key way, with U.S. government bond yields falling sharply.

But the reason for the drop is an unnerving one: Investors appear to be more on edge about the outlook for the economy.

Treasury Secretary Scott Bessent has said that the Trump administration considers the 10-year Treasury yield a benchmark of its success in lowering rates. The yield tracks the rate of interest the government pays to borrow from investors over 10 years and has dropped since mid-January, to around 4.2 percent from 4.8 percent. The decline in February was the steepest in several months.

The administration is targeting the 10-year yield because it underpins borrowing costs on mortgages, credit cards, corporate debt and a host of other rates, making it arguably the most important interest rate in the world. As it drops, that should filter through the economy, making many types of debt cheaper.

Unlike the short-term interest rate that is set by the Federal Reserve, the 10-year yield is a market rate, meaning that nobody has direct control over it. Instead, it reflects investors’ views on the economy, inflation, the government’s borrowing needs and changes the Fed may make to its rate in the years ahead.

That’s why the drop in February is troubling, analysts say. It shows, at least in part, that bond investors are growing gloomy about the economic outlook — and quickly.

“The market is pricing a growth scare,” said Blerina Uruci, chief U.S. economist at T. Rowe Price.

A better outcome would be for the declining 10-year yield to reflect slowing inflation, the prospect of more rate cuts by the Fed and a shrinking deficit that would require less government borrowing — all while the economy remains strong.

Instead, inflation expectations have risen this year amid worries that Mr. Trump’s tariff plans, alongside mass deportations, could reignite price increases throughout the economy. Stubborn inflation means the interest rates controlled by the Fed are likely to stay elevated for longer. Some analysts and investors fear that this could weigh on the economy until it cracks and the central bank is pushed into rapidly lowering rates.

So, if you can’t say you’re cutting all these things to end runaway government spending, try not reporting it. That might work, right? This is from the relentlessly brave AP. “The Trump administration may exclude government spending from GDP, obscuring the impact of DOGE cuts.” That way, no one, including economists, can possibly know what is happening. Let’s hope the Federal Reserve can remain independent and report US data if the Labor and Commerce Department can’t.

So, if you can’t say you’re cutting all these things to end runaway government spending, try not reporting it. That might work, right? This is from the relentlessly brave AP. “The Trump administration may exclude government spending from GDP, obscuring the impact of DOGE cuts.” That way, no one, including economists, can possibly know what is happening. Let’s hope the Federal Reserve can remain independent and report US data if the Labor and Commerce Department can’t.

Commerce Secretary Howard Lutnick said Sunday that government spending could be separated from gross domestic product reports, in response to questions about whether the spending cuts pushed by Elon Musk’s Department of Government Efficiency could possibly cause an economic downturn.

“You know that governments historically have messed with GDP,” Lutnick said on Fox News Channel’s “Sunday Morning Futures.” “They count government spending as part of GDP. So I’m going to separate those two and make it transparent.”

Doing so could potentially complicate or distort a fundamental measure of the U.S. economy’s health. Government spending is traditionally included in the GDP because changes in taxes, spending, deficits and regulations by the government can impact the path of overall growth. GDP reports already include extensive details on government spending, offering a level of transparency for economists.

Musk’s efforts to downsize federal agencies could result in the layoffs of tens of thousands of federal workers, whose lost income could potentially reduce their spending, affecting businesses and the economy at large.

Yahoo Finance, a good place to stalk the markets, has this report on what’s going on as I write. “Stock market today: Dow, S&P 500, Nasdaq slide as Trump tariffs stalk markets.”

Yahoo Finance, a good place to stalk the markets, has this report on what’s going on as I write. “Stock market today: Dow, S&P 500, Nasdaq slide as Trump tariffs stalk markets.”

US stocks retreated on Monday as a looming deadline fueled uncertainty around President Donald Trump’s tariff plans and investors looked ahead to the monthly jobs report and key retail earnings.

The S&P 500 (^GSPC) fell 0.2% while the tech-heavy Nasdaq Composite (^IXIC) erased early morning gains to fall 0.4%, weighed down by shares of Nvidia (NVDA). The Dow Jones Industrial Average (^DJI) fell below the flat line, as the major US indexes came off a volatile week and a losing February.

Nvidia stock plummeted on Monday as reports surfaced that the tech giant’s AI chips are reaching China despite export controls.

March trading kicked off with investors encountering more questions than answers as tariff deadlines loom, the Federal Reserve’s next meeting fast approaches, and the US economy faces the test of disproving investors’ fears about growth. First quarter economic growth is expected to slide following a string of weaker-than-expected economic data.

Tariffs on Canada and Mexico are set to come into effect on Tuesday, with no indication that a planned March 4 implementation date will be pushed back again. While 25% duties are planned, Commerce Secretary Howard Lutnick hinted that they could be lower by describing it as a “fluid situation.” New tariffs on China are also due on March 4, with Beijing said to be eyeing retaliatory measures on US agricultural products.

Elsewhere, European leaders’ weekend effort to rally around Ukraine prompted traders to boost bets on a bump in defense spending in the region, lifting related stocks.

It’s a depressing time for us Dismal Scientists. It’s one thing to have something bad happen, like a black swan event, but to watch your own government tank a perfectly healthy economy is tough to watch. I’ve already dropped so many reads that I’m hitting a word count of 3600. I’ll give you a break while I go play a new little game I picked up. It’s a gorgeous little anime game where I’ve just reincarnated as a walking, talking Mushroom, and I can solve everyone’s problems! The bad guy is a fat real estate developer, and the place is inhabited by people with both human and furry animal traits. It’s my new sanctuary beside the Star Wars Series.

I’ve lived here in New Orleans for 30 years now, and this is the first Mardi Gras I’ve just sat out. Somewhat for health problems, as I took another little fall today while walking Temple, and I don’t see the neurologist until next week. It’s tough not trusting your legs. Also, there are MAGAs around town, and many of my friends have reported they’ve destroyed things in the yard and homes if they have any display of having voted for Kamala. This is on all the uptown routes. It’s all just really depressing.

So, you stay very safe, warm, and cozy as we continue this very dark year. XOXO

What’s on your reading and blogging list today?

My Jaded Crystal Ball

Posted: May 11, 2012 Filed under: Bailout Blues, Banksters, Equity Markets, financial institutions | Tags: Credit Default swaps, financial innovation, financing outside of TRACE, securitization 11 Comments Okay, this is wonky. I’ve been avoiding writing about securitization for awhile because it can even get the best of people that know financial markets. You may remember that some one asked me where the next bubble lurked and I said commodities. Now, that’s actually a dangerous place for a bubble because commodities are things you eat and things that make your house light up and your car run. The housing bubble pretty much wiped out middle class wealth in the west. What would a commodities bubble burst do in the right markets? Well, think Mad Max or at least The Grapes of Wrath. Conversely, it could lead to a massive drop in key prices like that of oil. Imagine that one!

Okay, this is wonky. I’ve been avoiding writing about securitization for awhile because it can even get the best of people that know financial markets. You may remember that some one asked me where the next bubble lurked and I said commodities. Now, that’s actually a dangerous place for a bubble because commodities are things you eat and things that make your house light up and your car run. The housing bubble pretty much wiped out middle class wealth in the west. What would a commodities bubble burst do in the right markets? Well, think Mad Max or at least The Grapes of Wrath. Conversely, it could lead to a massive drop in key prices like that of oil. Imagine that one!

Here’s some interesting finds from FT Alphaville on the securitization of commodities. It’s titled “The subpriming of commodities” for effect.

It’s always been common practice for commodity inventory to be financed by banks by being pledged as security for the loans in question.

The problem comes if such enterprises, instead of using the inventory for general business purposes, are encouraged to stockpile for the sole purpose of liquidity provision and the opportunity to punt on the underlying commodities themselves. It’s a process which arguably artificially pumps up demand for the underlying inventory.

Bundle all those loans together, meanwhile — ideally into a product that can be sold to buyside investors seeking exposure to commodities — and suddenly you’ve got a direct source of funding for an ever-more speculative game.

When it comes to the larger players, meanwhile, this arguably transcends ‘trade finance’ even further — especially if it involves the setting up of a large number of special purpose vehicles to accomplish the process.

Here, for example, are the thoughts of Brian Reynolds, chief market strategist at Rosenblatt Securities, regarding what’s going on:

A little more than a year ago we picked up on a trend that we termed the “sub-priming” of commodities. Wall Street has been increasingly been doing structured finance deals wrapped around commodities, and this has added a bid for them while also making them vulnerable to downdrafts.

We know that many equity investors think (or at least hoped) that, after the disastrous record of wrapping pipeline and telecom assets in the 1990’s and sub-prime housing in the last decade, financial market reforms such as Dodd-Frank would have eliminated structured finance as a macro driver. When Dodd-Frank was proposed it envisioned standardized derivatives being placed on exchanges and clearinghouse. We felt it would encourage more non-standardized, exotic, and opaque structures to be created, and in the two years since it was enacted that’s what seems to have happened.

Important trends indeed. Yet, as Reynolds also notes, they’re also very hard to quantify given they mostly occur off-balance sheet:

This process is virtually impossible to quantify. We know that’s a disappointment to equity investors who are used to dealing with voluminous information, but that’s the nature of structured finance. Many structured finance deals are private in nature. As such most people, even those in the credit markets, did not know the full extent of the structuring going on in the 1990’s or the last decade until those firms, which were trapped by “Special Purpose Vehicles” (SPVs), such as Enron, WorldCom and Citigroup, became forced sellers. But over the last year we’ve heard more and more anecdotal evidence of Wall Street increasingly structuring commodity deals, such as structured notes and swaps and even using commodities as collateral.

In Reynold’s opinion — even though he’s not a commodity expert per se — this activity significantly increases the risk of a sharp drop in oil in the coming year, especially since structured finance transactions usually come with caps and floors, which act as important support and resistance levels.

That’s an interesting analysis for oil or copper. However, what happens if the commodities in question happen to be food? The only place this used to happen significantly was the gold market. Actually, it’s understandable for oil too. But is Wall Street so hungry for financial innovation that they’re willing to bet the world’s food supply on it? Yes, of course. They’ve already done it several times. History teaches us that it drives the prices up to unreasonable and unsustainable levels that take all kinds of people down when prices collapse.

Here’s an interesting bit on a contango that happened in the wheat market that already led to a food price crisis in 2007-2008. This one had the Goldman Sachs brand all over it. Last year, a similar situation occurred with the Oil Market and the same player.

On Monday, April 11, Goldman Sachs told its clients to sell commodities, and the market reacted with a $4 tumble in the price of West Texas Intermediate (WTI) crude oil and sell offs in other commodities.

On Thursday, April 14, the leaders of the “BRICS” nations (Brazil, Russia, India, China and South Africa), meeting in Sanya, China, continued to press for a new world monetary system that has a much lower reliance on the dollar, and called for stronger regulation of commodity derivatives to dampen excessive volatility in food and energy prices.

We are in another commodity price run up, like that experienced in the 2005-2008 period. Such commodity price frenzies have devastating consequences for the world’s poor who, in some instances, already spend half of their income on food. Today, in the U.S. itself, the rise in the price of gasoline to more than $4 per gallon threatens an economy still struggling to free itself from the still lingering effects of the last bursting bubble.

It appears that the Western economic systems have become ever more volatile over the past decade. That is, bubbles, followed by severe contractions, are appearing more often and with increased severity. This is in stark contrast to the dampening of the business cycle we observed, and celebrated, in the 1980s and 1990s. So, what changed?

In Harper’s last July, Fredrick Kaufman wrote an article entitled The Food Bubble, which explained the reasons for the run up in agricultural commodity prices just prior to the ’08 financial meltdown and worldwide recession. The popular business media gave the article short shrift. But, most of what Kaufman observed as the causes of the commodity price run up in the ’05-’08 period is now being repeated, a short three years later.

I’m finding all this interesting as I watch Jamie Dimon squirm on the big hedge loss reported by JP Morgan. That’s the $2 billion mark to market loss that makes me thing we’re on the verge of 2007 redux. Specifically, the market concentration is incredible because “the whale” created a huge problem for tons of hedge funds. Also, the regulator appeared to be asleep at the switch. You remember are old friends the Credit Default Swaps?

99 per cent of all CDS trades live in an information warehouse called DTCC, to which the regulators of the banks have access in however much detail they want!!! What kind of regulator doesn’t go and look at the that, when the mere public, aggregated info shows this?

Go check out the accompanying graph.

Anyway, I’m not going to get long winded and all financial economist on you, but sheesh, how many times does history have to repeat itself in markets before we get some one to do something useful? I’m just reminded of all the little canaries that died on the way to the big 2007 blow up that people ignored. How many canaries have to die this time out before we get another big one

Vegas Gambling vs Wall Street Gambling

Posted: November 23, 2011 Filed under: Banksters, Economy, Equity Markets, financial institutions 5 CommentsOne of the things that has always struck me about folks that treat the financial sector like any other business venture is the lack of  understanding of what the finance sector really does. There are several basic functions if you read the literature. The banking industry originally evolved from goldsmiths that would safekeep gold for people. This eliminated the need for every one to keep a small army with them at all times to stop robbers from stealing all their gold. Goldsmiths eventually learned that a fairly sizable chunk of that gold never left their premises and found out they could lend some of it out for a return and not be caught short. That eventually lead them from being gold babysitters to lenders. Then, we eventually got around to trying to find some financial contracts that would help us if the worst happened by buying insurance. From these sets of agreements, we now have exotic derivatives, financial innovations, credit default swaps, and a host of other banking services. The basics things that the banking sector does is help you save or store up future purchasing power, borrow or lend purchasing power, and help move money around from place to place via the payment systems. That would be check clearing and ATMs and things like that. The Federal Reserve Bank was set up to handle that latter function but most of that function has been privatized since regional banks now clear checks and there are private clearing houses for Automated Payments. The Fed’s role is now fairly small. It still pushes cash from the US Mint/Treasury into the banking system and its FedWire system still handles a huge number of wire transfers between banks. If banks won’t lend to each other via the Fed Funds market, it is also available to lend money at the discount window. That used to be only available to member banks but it’s now open to a lot more institutions.

understanding of what the finance sector really does. There are several basic functions if you read the literature. The banking industry originally evolved from goldsmiths that would safekeep gold for people. This eliminated the need for every one to keep a small army with them at all times to stop robbers from stealing all their gold. Goldsmiths eventually learned that a fairly sizable chunk of that gold never left their premises and found out they could lend some of it out for a return and not be caught short. That eventually lead them from being gold babysitters to lenders. Then, we eventually got around to trying to find some financial contracts that would help us if the worst happened by buying insurance. From these sets of agreements, we now have exotic derivatives, financial innovations, credit default swaps, and a host of other banking services. The basics things that the banking sector does is help you save or store up future purchasing power, borrow or lend purchasing power, and help move money around from place to place via the payment systems. That would be check clearing and ATMs and things like that. The Federal Reserve Bank was set up to handle that latter function but most of that function has been privatized since regional banks now clear checks and there are private clearing houses for Automated Payments. The Fed’s role is now fairly small. It still pushes cash from the US Mint/Treasury into the banking system and its FedWire system still handles a huge number of wire transfers between banks. If banks won’t lend to each other via the Fed Funds market, it is also available to lend money at the discount window. That used to be only available to member banks but it’s now open to a lot more institutions.

Bankers usually make money by charging fees on their services, interest rates on their loans, and then they make arbitrage profits if they invest. For years, that last function wasn’t a big deal for bankers because laws stopped them from investing in anything very creative. Laws have changed a lot over the last 10-20 years and even if commercial banks can’t make risky investments, they are likely to be part of a bank holding company that owns some subsidiary that can. Allowing banks–who basically still have the role of “safekeeping”–to gamble has been a huge mistake. Besides the lax laws, they have had a lot of cheap cash available because of Greenspan’s relatively lose monetary policy during the last years of his tenure and they’ve been able to reduce their risk by having deposit insurance which covers their deposits in case of default. There has also been an increase in “financial innovations” and techniques which serve as pseudo insurance but generally come in the form of very hard-to-price assets so they can be risky. Many banks don’t use them just for hedging which is this risk management approach to their use. A lot of banks just plan gamble. We’ve definitely seen banks misjudge risk and rely heavily on what I would consider gambling activities.

So, I’ve worked back of the house at a casino and I’ve worked in banking and of course, I’m a financial economist so I’ve got a little knowledge and experience on all fronts. The one thing that I will say about gambling in a casino is that a good time is had by all, every one understands it’s gambling, and the gambling industry hires a lot of people in the process that do fairly straightforward jobs. They only get tips if the customers say so. Bonuses for random wins are de rigueur in the finance sector. Silly thing is that most financiers think they’ve actually earned those bonuses for doing some miracle. There’s a few good reads to let you know exactly how misguided they are on their opinions of their skills. The first is anything by Nassim Nicholas Taleb who is a practitioner of financial mathematics and a former Wall Street trader. His book “Fooled by Randomness” is just full of examples of the fallacies that drive Wall Street Bankers into thinking too highly of themselves and paying themselves based on gambling and randomly hitting the jackpot. You can also read anything by Nobel Prize winner Daniel Kahneman. Actually, you can watch them both talk about these things in a video at Edge in a program called Reflections on a Crisis.

Kahneman explains why there are bubbles in the financial markets, even though everyone knows that they eventually burst. The researchers used the comparison with the weather: If there is little rain for three years, people begin to believe that this is the normal situation. If over the years stocks only increase, people can’t imagine a break in this trend.

Taleb speaks out sharply against the bankers. The people in control of taxpayer’s money are spending billions of dollars. “I want those responsible for the crisis gone today, today and not tomorrow,” he says, leaning forward vigorously. The risk models of banks are a plague, he says, the bankers are charlatans.

It is nonsense to think that we can assess risks and thus protect against a crash. Taleb has become famous with his theory of the black swan described in his eponymous bestsellers described. Black swans, which are events that are not previously seen–not even with the best model. “People will never be able to control a coincidence,” he says.

Okay, so that’s actually the background to something I want to point you to on VOXEU called “What is the contribution of the financial sector?” by Andrew Haldane. I think it’s a good thing to look at because we need to establish some basic knowledge and laws that separate the speculative activities from the banking activities that actually may provide value. (Although I still could argue that privatizing the payments system may prove risky and foolish some day, there are some things that banks do that are useful.) This way we can see the damage done when so many politicians essentially empower the gambling aspects. Another offshoot is our tax policy which favorably treats capital gains without any reference to the source of the profit. People that run businesses that enhance economic welfare of every one are taxed at the same favorable rate as those that basically gamble resources away. That’s a very bad incentive system. Haldane points out the difference between managing risk of financial contracts and risk-taking that is basically gambling and how much of the Western nation’s financial sector has morphed more into a gambling sector than a financial services provider.

But crisis experience has challenged this narrative. High pre-crisis returns in the financial sector proved temporary. The return on tangible equity in UK banking fell from levels of 25%+ in 2006 to – 29% in 2008. Many financial institutions around the world found themselves calling on the authorities, in enormous size, to help manage their solvency and liquidity risk. That fall from grace, and the resulting ballooning of risk, sits uneasily with a pre-crisis story of a shift in the technological frontier of banks’ risk management.

In fact, high pre-crisis returns to banking had a much more mundane explanation. They reflected simply increased risk-taking across the sector. This was not an outward shift in the portfolio possibility set of finance. Instead, it was a traverse up the high-wire of risk and return. This hire-wire act involved, on the asset side, rapid credit expansion, often through the development of poorly understood financial instruments. On the liability side, this ballooning balance sheet was financed using risky leverage, often at short maturities.

This is an important statement because not only did political institutions loosen laws or not put in place laws to stop this from happening, but when it happened, we all paid and they’ve ignored how costly this was to every one else. Plus, they keep wanting us to sacrifice instead of the people that broke the economic growth machine. The basic narrative is that these folks gambled with others’ money and the government had to pay the house. This is wrong in every sense of what is and isn’t moral. Haldane argues that risk-taking is not a value-added activity for banks and backs it up with empirical evidence.

The financial system provides a number of services to the wider economy, including payment and transaction services to depositors and borrowers; intermediation services by transforming deposits into funding for households, companies or governments; and risk transfer and insurance services. In doing so, financial intermediaries take on risk. For example, when they finance long-term loans to companies using short-term deposits from households, banks assume liquidity risk. And when they extend mortgages to households, they take on credit risk.

But bearing risk is not, by itself, a productive activity. The act of investing capital in a risky asset is a fundamental feature of capital markets. For example, a retail investor that purchases bonds issued by a company is bearing risk, but not contributing so much as a cent to measured economic activity. Similarly, a household that decides to use all of its liquid deposits to purchase a house, instead of borrowing some money from the bank and keeping some of its deposits with the bank, is bearing liquidity risk.

Neither of these acts could be said to boost overall economic activity or productivity in the economy. They re-allocate risk in the system but do not fundamentally change its size or shape. For that reason, statisticians do not count these activities in capital markets as contributing to activity or welfare. Rightly so.

What is a demonstrably productive economic activity is the management of risk. Banks use labour and capital to screen borrowers, assess their creditworthiness and monitor them. And they spend resources to assess their vulnerability to liquidity shocks arising from the maturity mismatches on their balance sheets. Customers, in turn, remunerate banks for these productive services.

The current framework for measuring the contribution of financial intermediaries captures few of these subtleties. Crucially, it blurs the distinction between risk-bearing and risk management. Revenues that banks earn as compensation for risk-bearing – the spread between loan and deposit rates on their loan book – are accounted for as output by the banking sector. So bank balance-sheet expansion, as occurred ahead of the crisis, counts as increased value-added. But this confuses risk-bearing with risk management, especially when the risk itself may be mis-priced or mis-managed.

Markets (e.g. Herds of PEOPLE) aren’t very Rational a Lot of the Time

Posted: September 24, 2011 Filed under: Economy, Equity Markets | Tags: behavioral economics, behavioral finance, rational markets 7 Comments

The Confidence Fairy is coming for your Savings!!!

One of the primary reasons I didn’t do an investments specialization for my PHD in financial economics is the overwhelming and pervasive group think on Rational Expectations or what’s called the Efficient Market Hypothesis. I’ve never really bought into this. I think it is more an occasional circumstance or specific market behavior at that point when everything is going just dandy which is why I am more the sunspot equilibrium type. I never found compelling reasons for the efficient markets view to be considered an overarching framework for all circumstances. That kind of unorthodox outlook doesn’t buy you much print space in finance journals which means no tenure for you cupcake!! (Although for some reason I can get it passed reviewers when it’s couched in the term “bubble” which is so very sunspot.)

Economists have become a little more accepting of the warts and faults inherent in the hypothesis–notice it is still a hypothesis and not a theory–but finance people still have a tendency to worship at its alter. Economists started out as philosopher social scientists–which is also why the big money is in finance–so they’re a little more open to the idea that markets aren’t all that efficient all the time. I linked to the Wikipedia explanation of the idea for you which is adequate for our purposes. The deal is when you build rational expectations into an economics model or investment model this is what you assume.

To assume rational expectations is to assume that agents‘ expectations may be individually wrong, but are correct on average. In other words, although the future is not fully predictable, agents’ expectations are assumed not to be systematically biased and use all relevant information in forming expectations of economic variables.

This basically rules out wrong group think that won’t deny “relevant information”. If that was the case in reality, there would be no holocaust deniers, evolution deniers, climate change deniers, or flat earthers of substantial numbers to influence the average. Basically, we’d have to accept the “average” rationality of today’s Republican Party and given the existence, electability and popularity of Rick Santorum, Michelle Bachmann, and Ron Paul, I’ll rest my case and reject that. We have a major political party that’s basically a cult of irrationality these days.

There are two really important real life phenomenon that make that assumption look really bad in finance research. One is a little paradox called the Home Bias Puzzle where research has basically shown that most people will still buy investments from their own country despite the availability of better deals abroad. The second is momentum. This is the pack animal behavior in the market where you see something hit the market and suddenly every one is moving that direction when it doesn’t make much sense on a fundamentals level. This is when I sell all my stock holdings. The little voice inside of me will go: “wtf is this rally for? The economy isn’t all that great! I think I better get out of here before they realize they’re all on something!” This is how I’ve managed to remove my “ass”ets and avoid the major crashes since way back in the 1980s.

Whenever you get a financial crises or financial bubbles, you tend to get the panicked cow phenomenon in that if one is spooked the rest chase wildly along. They’ve even programed this behavior into their computers oddly enough. Oh, and btw, none of the strategies and no market guru like Cramer or Buffet or Jesus your neighborhood grocer could ever be right and beat the market consistently if the financial markets were truly rational and efficient. That’s another story, just accept my word for it right now.